The News: Nvidia reported first-quarter earnings after the bell on Wednesday. The stock fell over 1% in after-hours trading after losing a little more than 2% on the day. Here’s how it did:

- EPS: $1.80, adjusted

- Revenue: $3.08 billion

Wall Street had anticipated adjusted earnings per share of $1.69 on revenue of $3 billion, according to Refinitiv consensus estimates. However, it’s difficult to compare reported earnings to analyst estimates as the coronavirus pandemic continues to affect global economies and makes earnings impact difficult to assess. Read the full earnings news piece from CNBC.

Analyst Take: This quarter proved to be very solid for NVIDIA. While hitting on both earnings and revenue targets alone are always a sound result, the quarter also included the acquisition of Mellanox, which will be an important piece to the long-term NVIDIA datacenter growth strategy. Additionally, the announcement of Cumulus Networks, added to its open source software for networking and AI portfolio. Another feather in NVIDIA’s proverbial cap.

Some of the overall financial results that caught my attention were the company’s solid YoY growth at 39% as well as its big increase in gross margin, operating income, net income, diluted EPS and Cash Flow from operations. Income grew both gross and net by over 100%. A tremendous year over year feat. It is important to note, those results weren’t as big on a QoQ basis, but NVIDIA has a well defined seasonality to it, so I tend to look to the YoY data to get a more acute sense of the business.

Exploring NVIDIA by Segment

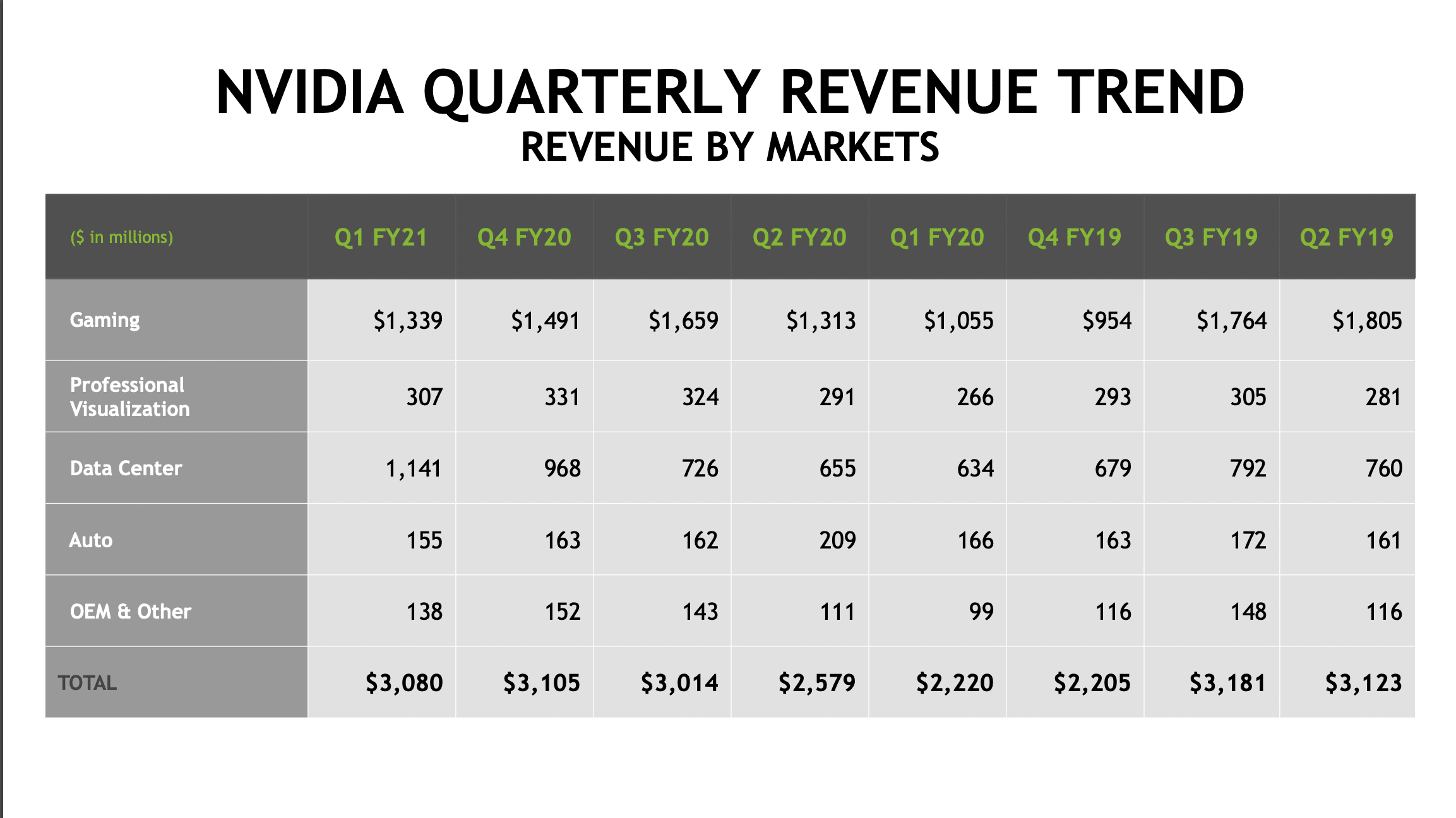

On a segment by segment basis, the company also showed strong YoY growth in all segments, with only automotive seeing a slight decline for obvious reasons related to Covid-19. There was a long list of NVIDIA highlights for the quarter that included significant design wins for NVIDIA GeForce, its first $1 Billion+ quarter in Data Center and a plethora of other results.

For a full listing of the quarters highlights, visit the NVIDIA quarterly press release.

While there were many solid advancements in technology across the segments, the story of this quarter was all about the data center. Not only did it break $1.14 Billion in revenue, but that represented YoY growth of 80 percent–a staggering result that will only be accelerated by the completion of the Mellanox acquisition, which will reflect in the next quarters earnings.

Additionally, in data center, the company had a plethora of news come out of its GTC Virtual Conference. This included enhancements to its recommender framework with Merlin, advancements in conversational AI with Jarvis, a massive update to its data center GPU, with the A100 based on next generation NVIDIA Ampere Architecture and more including a DGX system based on the aforementioned A100. For more on this, check out my coverage of GTC here.

NVIDIA Makes Significant Contributions to Covid

This quarter, I highlighted many companies contributions to Covid-19 through podcasts and research notes, however, I hadn’t had a chance yet to share what NVIDIA was working on. The company had a long list of contributions that are worth noting and the continued support of its HPC, GPU and AI capabilities are noteworthy.

COVID-19 Efforts

- NVIDIA and its employees have committed to donate more than $10 million to those affected during this period.

- Accelerated promotions and raises for employees by several months.

- Released AI models in collaboration with the National Institutes of Health to help researchers detect COVID-19 in lung scans.

- Joined the White House’s COVID-19 High Performance Computing Consortium, alongside leaders from the U.S. government, industry and academia, to accelerate COVID-related research.

- Provided a free 90-day license to NVIDIA Parabricks™, a genomics software stack that uses GPUs to accelerate the analysis of gene-sequencing data, to researchers working on COVID-related topics.

I also found CEO Jensen Huang’s commitment to its workforce encouraging. For those that missed the news, the company pulled forward its salary increases and committed to no workforce reductions throughout the ongoing pandemic. A sound move for the culture and advancement of NVIDIA.

NVIDIA Q2 Forward Looking Guidance

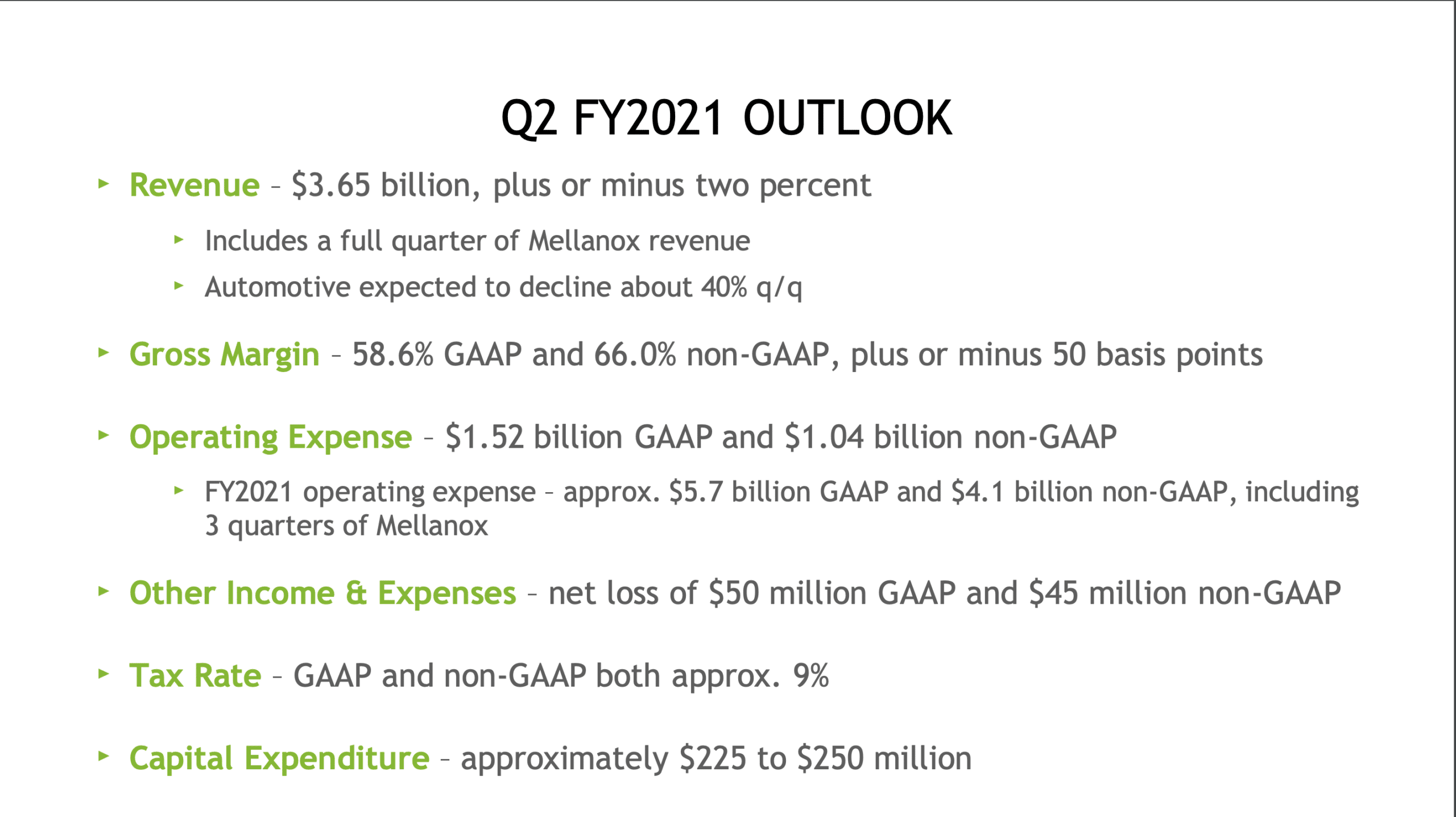

Going forward, NVIDIA seems to have a good handle on its next quarter, announcing in its earnings presentation an expected revenue of $3.65 Billion. The biggest risks, it shared, come in automotive, which has understandably seen a pull back.

This overall revenue looks impressive over an 8 quarter period, but again, it must be noted that Mellanox will be represented in that number and has over a $1 Billion annual run rate. That still looks to be a very strong quarter for NVIDIA, and will be important to watch for YoY growth continuing in key segments data center and gaming.

Overall Impressions of NVIDIA Q1 Earnings

NVIDIA should be pleased with the results of the quarter. The strong sales in key categories were driven by a number of factors, but with commerce and services continuing to make big investments in AI, including recommender and conversational, it is clear that NVIDIA technology sits behind much of these advancements. The launches at GTC will continue to propel the company in this space and put pressure on rivals to advance AI initiatives, which will be good for competitive reasons.

I also believe, given these tumultuous times, that gaming stands to continue to perform well, and the company’s continued wins in lower end gaming laptops will bare fruit in the coming periods, while its streaming game service GeForce Now will be another revenue category to watch.

While we are not out of the woods as it pertains to Covid-19, NVIDIA appears well positioned to deal with this regardless of how long it persists. Q2 was unequivocally a bang up result for NVIDIA. Now we watch to see if this type of momentum can be maintained.

Futurum Research provides industry research and analysis. These columns are for educational purposes only and should not be considered in any way investment advice.

Read more analysis from Futurum Research:

Nvidia has Become a Power Broker for the Next Wave of Datacenter Technology

Cisco Delivers Above Expectations for Q3 Despite Headwinds

Microsoft Azure Scoops up Metaswitch in Bid to Make Azure the Meta-5G Edge Cloud

Image: Microsoft

Author Information

Daniel is the CEO of The Futurum Group. Living his life at the intersection of people and technology, Daniel works with the world’s largest technology brands exploring Digital Transformation and how it is influencing the enterprise.

From the leading edge of AI to global technology policy, Daniel makes the connections between business, people and tech that are required for companies to benefit most from their technology investments. Daniel is a top 5 globally ranked industry analyst and his ideas are regularly cited or shared in television appearances by CNBC, Bloomberg, Wall Street Journal and hundreds of other sites around the world.

A 7x Best-Selling Author including his most recent book “Human/Machine.” Daniel is also a Forbes and MarketWatch (Dow Jones) contributor.

An MBA and Former Graduate Adjunct Faculty, Daniel is an Austin Texas transplant after 40 years in Chicago. His speaking takes him around the world each year as he shares his vision of the role technology will play in our future.