Analyst: Olivier Blanchard, Brendan Burke

Publication Date: June 29, 2026

What Is Covered in This Article:

- Qualcomm’s strategic transition into a comprehensive, full-stack AI platform provider.

- Aggressive fiscal 2029 financial targets focusing on diversified non-handset revenue growth.

- The company’s entry into the high-performance data center market, led by the new Dragonfly portfolio and the acquisition of Modular.

- Expansion and acceleration of Qualcomm’s automotive design-win pipeline and long-term revenue milestones.

- Emerging opportunities in IoT, robotics, and the Physical AI ecosystem.

- Qualcomm’s most critical opportunities and threats in the era of AI inference and agentic workloads

The Event—Qualcomm’s Pivotal Shift into the Agentic Era: At its 2026 Investor Day event on June 24 in New York, Qualcomm provided some color on the evolution of its corporate trajectory, which, as you may recall, initially began as a diversification effort into mobile-adjacent verticals and automotive, but quickly evolved into an ambitious full-stack AI strategy. Long recognized as a leader in connectivity IP and mobile handset silicon (particularly in the flagship and premium tiers), Qualcomm has since formally signaled its transition into a comprehensive, full-stack platform provider spanning the entire compute continuum, driven in great part by the many engineering challenges of the Agentic AI era, which Qualcomm is uniquely positioned to solve.

This strategic pivot repositions the organization to capture a massive total addressable market (TAM) projected to reach approximately $1.7 trillion by 2030. Over the next three to five years, Qualcomm anticipates critical technological inflection points across data center infrastructure, automotive systems, industrial robotics, and next-generation edge devices. This is welcome news, as one of the company’s primary objectives on the 24th was to articulate how it would continue to deliver significant growth amid the prospect of a sluggish Mobile market, an increasingly stressed PC market, and a mercurial automotive market. The answer was, of course, AI, but Qualcomm needed not only to provide a credible plan of action but also to stick the landing. Execution will be another story, but so far, so good.

Redefining the Financial Horizon: Updated Fiscal 2029 Targets

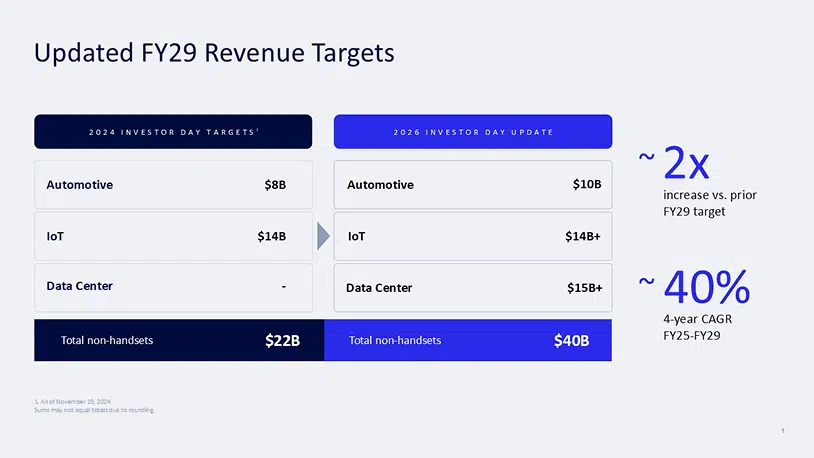

The primary indicator of Qualcomm’s confidence in its diversification strategy lies in its aggressive upward revisions for its QCT semiconductor business segment. Most notably, the company doubled its previously stated expectations for diversified growth.

- Non-Handset Revenues: Raised to $40 billion by fiscal 2029, representing an approximate 2x increase over the company’s prior long-term targets.

- Handset Rebalancing: In a historic shift for the business model, handset revenues are projected to comprise only one-third of total QCT revenues by fiscal 2029, mitigating the company’s historic exposure to mobile-only market cycles.

- Earnings Power: Qualcomm is targeting a non-GAAP diluted earnings per share (EPS) of more than $18.00 for fiscal 2029, establishing a robust long-term growth and operating leverage framework.

Figure 1: Updated FY29 Revenue Targets

Broken down into their individual categories, Qualcomm’s updated fiscal 2029 targets for its QCT business come down to:

- Non-handset revenues: $40 billion by fiscal 2029

- Automotive revenues: $10 billion by fiscal 2029

- IoT revenues: >$14 billion by fiscal 2029

- Industrial, networking, and robotics: $8 billion

- Personal AI and Compute: $6 billion

- Data Center revenues: More than $15 billion by fiscal 2029

- Handset Revenues: Should represent only 1/3 of QCT revenues by fiscal 2029

Core Pillars of Qualcomm’s Diversification Strategy

Per Qualcomm, “multiple large markets are reaching inflection points, as AI compute becomes increasingly distributed across devices, edge and cloud over the next 3-5 years, including agent-ready edge devices, data center infrastructure, automotive, industrial systems, networking and robotics” for a combined total addressable market (TAM) of roughly $1.7 trillion by 2030.

Looking beyond that fiscal horizon, Qualcomm is zooming in on that growth, particularly in data center, robotics, ADAS / autonomous driving, industrial AI, personal AI, and 6G. Qualcomm’s theory of the case is that the era of agentic AI will drive a new upgrade cycle across all intelligent connected device surfaces, which aligns perfectly with the company’s targeted diversification strategy and somewhat prescient R&D roadmap.

Three areas in particular need a bit of additional attention – Data Center, Automotive, and IOT:

1. Disrupting the Data Center AI Infrastructure

Qualcomm’s most ambitious new frontier is its ambitious entry into the high-performance data center market. The company unveiled a comprehensive data center AI infrastructure strategy, supported by the new Qualcomm Dragonfly-branded portfolio.

- The Goal: Achieve more than $15 billion in data center revenues by fiscal 2029.

- Strategic Partnerships: Bolstering this roadmap are high-profile collaborations, including a multi-generation agreement with Meta to develop next-generation data center CPUs, alongside a deepened relationship with Hugging Face to optimize open, developer-driven AI from edge to cloud.

- Inorganic Growth: Qualcomm also announced the acquisition of Modular, a move designed to strengthen its unified software stack and developer tooling – potentially closing one of the most glaring gaps in the company’s AI ambitions, particularly relative to NVIDIA’s CUDA.

For a deeper dive into this critical section of Qualcomm’s presentation and data center strategy, read our companion report, Qualcomm’s Data Center Reentry at Investor Day 2026 Arrives Just in Time for the Inference Decode Prize.

2. Scaling the Automotive Design-Win Pipeline

While not as much a point of focus during this year’s event, the automotive sector nevertheless continues to be an extraordinary growth engine for Qualcomm’s intelligent connected platform. Through its integrated Snapdragon Digital Chassis offering, the company has secured an impressive competitive moat.

Two data points stood out to us during the presentation: The first touches on the state of Qualcomm’s design-win pipeline, which expanded to an impressive $65 billion. The second is a revenue milestone, with targets for the automotive sector being raised to $10 billion annually by fiscal 2029, which, if memory serves, is well ahead of schedule.

3. Monetizing IoT, Robotics, and Physical AI

Beyond automotive and data centers, the broader internet of things (IoT) ecosystem is also experiencing an AI-driven revolution, albeit not quite yet at the pace and scale of the data center segment. Nevertheless, Qualcomm expects its IoT segment as a whole to generate more than $14 billion in revenue by fiscal 2029, subdivided into high-impact industries:

- Industrial, Networking, and Robotics ($8 billion target): One of the more interesting opportunities for Qualcomm is in the inbound “Physical AI” wave, where enterprise robotics and smart manufacturing require processing power at the local edge. While competitors like NVIDIA, Tesla, NXP, and Texas Instruments have invested early in robotics R&D and are quickly establishing themselves among the leaders in the field, Qualcomm’s opportunity here could be significant. And while we are still a few years away from any kind of momentum at scale for the segment, it is clear that the combination of Qualcomm’s edge compute, AI, advanced connectivity, IOT, and automotive IP will help drive the company’s physical AI efforts. And given how aligned essential robotics technologies are with automotive technologies, Qualcomm’s full-stack automotive portfolio should read as a top-line signal that, while generally quiet about it now, Qualcomm will be a major player in that space.

- Personal AI and Compute ($6 billion target): Capitalizing on the proliferation of AI-capable laptops, PCs (such as the Snapdragon X Elite platforms), and next-generation intelligent devices. My interest here is less on AI PC and more on XR – or rather, agentic glasses. Expect a broader discussion about the category in a separate note, but for now, keep in mind that Qualcomm’s XR IP continues to help drive the XR market forward, which is itself expanding at a >20% CAGR. While we remain somewhat bearish about augmented and mixed reality going from niche to mainstream anytime soon, smart glasses (now transitioning into “agentic glasses) continue to capture more market share year-on-year, thanks to relatively accessible price-points, decent interoperability, ease of use, and useful everyday features. We believe that as more conversational, agentic features make their way into the category and utility increases, more consumers will embrace the convenience of using their mobile devices’ most popular features (camera, audio, search, calendar, navigation, and messaging) hands-free when away from their desk or couch.

Strategic Implications: The Rise of Agentic AI

According to President and CEO Cristiano Amon, Qualcomm is moving aggressively beyond pure silicon manufacturing to establish itself as a full-stack platform enterprise. As mentioned earlier, the catalyst for this transformation is Agentic AI—autonomous, context-aware AI agents that require massive low-power processing distributed across the edge and the cloud. Qualcomm’s structural advantage lies in its historical expertise in delivering high-performance, low-power computing and advanced connectivity. And as AI inference workloads shift away from centralized cloud models toward distributed, hybrid environments, Qualcomm finds itself uniquely positioned to help drive the hardware refresh cycle in both consumer and commercial segments, much as NVIDIA was perfectly positioned to capitalize on the Model training opportunity.

Management notes that “agent-ready” edge devices will trigger a significant upgrade cycle opportunity over the coming years, sustaining demand across consumer and industrial tiers alike, and we agree with that assessment, particularly as the monetization of tokens in the cloud drives AI users toward more cost-effective alternatives.

Forward-Looking Execution Risks

While Qualcomm’s financial outlook leans towards optimism, management’s commentary acknowledges a number of structural headwinds that will require careful navigation: For starters, the successful execution of this 3-to-5-year roadmap will rely, in part, on navigating a cyclical semiconductor environment, mitigating a heavy historical concentration of business within China, and managing ongoing geopolitical trade tensions.

But perhaps more importantly, expanding beyond Qualcomm’s familiar Edge segments will require the companies to push into already fairly entrenched enterprise data center ecosystems, where competition is fierce. That said, the AI industry’s transition from a primarily training-centric, GPU-heavy focus that drove the first few waves of AI and data center investments to an inference-prioritizing, CPU-heavy focus is Qualcomm’s opening. Inference will become a volume play, and Qualcomm’s impressive performance-per-watt IP, both in edge and data center environments, provides the company with an attractive hardware story. Qualcomm’s acquisition of Modular, which includes onboarding Chris Lattner, could certainly provide it with the AI software stack it needs to achieve the kind of adoption that NVIDIA enjoyed, in great part thanks to CUDA.

Backed by proven operating leverage and landmark ecosystem agreements with hyperscalers like Meta, Qualcomm’s updated fiscal 2029 guidance underscores an organization successfully transforming its identity from an Edge-first semiconductor market leader into a more foundational computing architecture leader for the distributed AI era.

You can recap the event at Qualcomm’s Investor Relations site.

What to Watch:

- Execution of the “Dragonfly” data center portfolio, specifically tracking design wins and revenue milestones against the $15 billion fiscal 2029 target.

- The success of Qualcomm’s integration of Modular’s software stack to deliver a credible parallel to NVIDIA’s CUDA for AI developers.

- Progress in the automotive design-win pipeline, currently valued at $65 billion, as the company works toward its $10 billion annual revenue goal by 2029.

- Adoption rates of “agent-ready” edge devices and XR smart glasses, assessing whether consumer demand shifts toward agentic, hands-free features as anticipated.

- Management’s ability to navigate geopolitical trade tensions and concentration risks in the Chinese market while balancing cyclical semiconductor headwinds.

- More partnership announcements and wins beyond Meta in the hyperscaler ecosystem – especially in decode use cases, where Qualcomm could establish itself as a category leader.

Disclosure: Futurum is a research and advisory firm that engages or has engaged in research, analysis, and advisory services with many technology companies, including those mentioned in this article. The author does not hold any equity positions with any company mentioned in this article.

Analysis and opinions expressed herein are specific to the analyst individually and data and other information that might have been provided for validation, not those of Futurum as a whole.

Other Insights From Futurum:

Qualcomm Q2 FY 2026 Earnings Show Data Center Entry and Auto Strength

Qualcomm Q1 FY 2026 Earnings: Record Revenue, Memory Headwinds

Featured Image: Qualcomm

Author Information

Olivier Blanchard is Research Director, Intelligent Devices. He covers edge semiconductors and intelligent AI-capable devices for Futurum. In addition to having co-authored several books about digital transformation and AI with Futurum Group CEO Daniel Newman, Blanchard brings considerable experience demystifying new and emerging technologies, advising clients on how best to future-proof their organizations, and helping maximize the positive impacts of technology disruption while mitigating their potentially negative effects. Follow his extended analysis on X and LinkedIn.

Brendan is Research Director, Semiconductors, Supply Chain, and Emerging Tech. He advises clients on strategic initiatives and leads the Futurum Semiconductors Practice. He is an experienced tech industry analyst who has guided tech leaders in identifying market opportunities spanning edge processors, generative AI applications, and hyperscale data centers.

Before joining Futurum, Brendan consulted with global AI leaders and served as a Senior Analyst in Emerging Technology Research at PitchBook. At PitchBook, he developed market intelligence tools for AI, highlighted by one of the industry’s most comprehensive AI semiconductor market landscapes encompassing both public and private companies. He has advised Fortune 100 tech giants, growth-stage innovators, global investors, and leading market research firms. Before PitchBook, he led research teams in tech investment banking and market research.

Brendan is based in Seattle, Washington. He has a Bachelor of Arts Degree from Amherst College.