Analyst(s): Keith Kirkpatrick

Publication Date: June 3, 2026

Document #: AIOKK202606

The excitement around AI-assisted development suggests companies can now generate their own applications instead of buying expensive SaaS platforms. However, the evidence shows that AI’s true value lies not in replacing core systems, but in extending the operational depth, governance, and ecosystem integration that enterprise SaaS platforms already provide.

Key Points

- AI is clearly influencing software architecture and vendor evaluations, but the evidence does not support a simplistic conclusion that enterprises are abandoning SaaS platforms for AI-built substitutes.

- AI-assisted development can rapidly produce prototypes, utilities, and lightweight workflow tools, but it does not replace the operational maturity, governance, integration depth, and domain expertise embedded in enterprise SaaS platforms.

- The real value of enterprise SaaS sits below the interface, within data orchestration, cross-platform workflows, compliance, security, operational hardening, and embedded best practices that are difficult to recreate quickly with AI-native development tools.

- The strongest strategic use case for AI-native tools is extension rather than substitution: enterprises should buy core systems of record and use AI to accelerate customization, integrations, role-specific tools, dashboards, and lightweight workflow enhancements around those platforms.

- Avoid using AI for the wrong applications. As systems approach core processes, regulated data, or organizational dependency, mistaking functional code for a production-ready platform becomes increasingly hazardous.

Recommendations

- Package AI as Augmentation, Not a Rip-and-Replace Narrative: Because SaaS-to-SaaS switching remains a larger driver than AI replacement in most categories, vendors should position AI as a way to compress cycle time, reduce service costs, and extend existing workflows while protecting the core platform relationship.

- Make Extension a First-Class Product Strategy: SaaS vendors should invest aggressively in APIs, low-code/no-code tooling, agent builders, SDKs, and AI-assisted customization layers. The goal should be to make ‘build around us’ easier, safer, and more economically attractive than ‘build instead of us’.

- Position Around Operational Depth, Not Just Features: Vendors should sharpen messaging around what customers actually buy: governance, uptime, compliance, security, orchestration, data quality, and business continuity. The strongest defense against ‘we can build this ourselves’ is proving the hidden complexity that customers would otherwise inherit.

- Use Customer Data and Workflow Context to Strengthen Platform Gravity: Vendors should connect AI roadmaps to the data models, identity layers, workflow histories, and ecosystem integrations that already make platforms sticky.

- Treat AI Governance as a Competitive Moat: As agentic AI adoption grows, vendors should differentiate on permissioning, observability, human-in-the-loop controls, auditability, escalation paths, and policy enforcement. Governance will increasingly be a formal buying criterion rather than a technical afterthought.

Analysis

The excitement around AI-assisted development has created a powerful new story in enterprise software: that companies can now generate their own applications in hours instead of buying expensive SaaS platforms that took years to implement. Tools such as Cursor, Replit, GitHub Copilot, and Bolt have made that idea feel plausible because they can, in fact, produce working prototypes, simple apps, and focused utilities with remarkable speed.

For enterprise buyers under pressure to control software costs, improve ROI, and simplify bloated application portfolios, the promise of ‘just build it yourself’ is understandably appealing. With enterprise software spending continuing to climb and many organizations frustrated by the gap between expected and realized returns, AI-generated applications may appear to be a compelling alternative to another large, multi-year SaaS commitment. Consolidation pressures only make that temptation stronger, as buyers increasingly question whether they truly need every module from every vendor.

The most recent ETR SaaS displacement data published in February 2026 highlights an important distinction: AI is clearly influencing software architecture and vendor evaluations, but the evidence does not support a simplistic conclusion that enterprises are abandoning SaaS platforms for AI-built substitutes. Instead, AI is more often showing up as an augmentation layer, a customization accelerator, or a catalyst for platform consolidation and SaaS-to-SaaS switching.

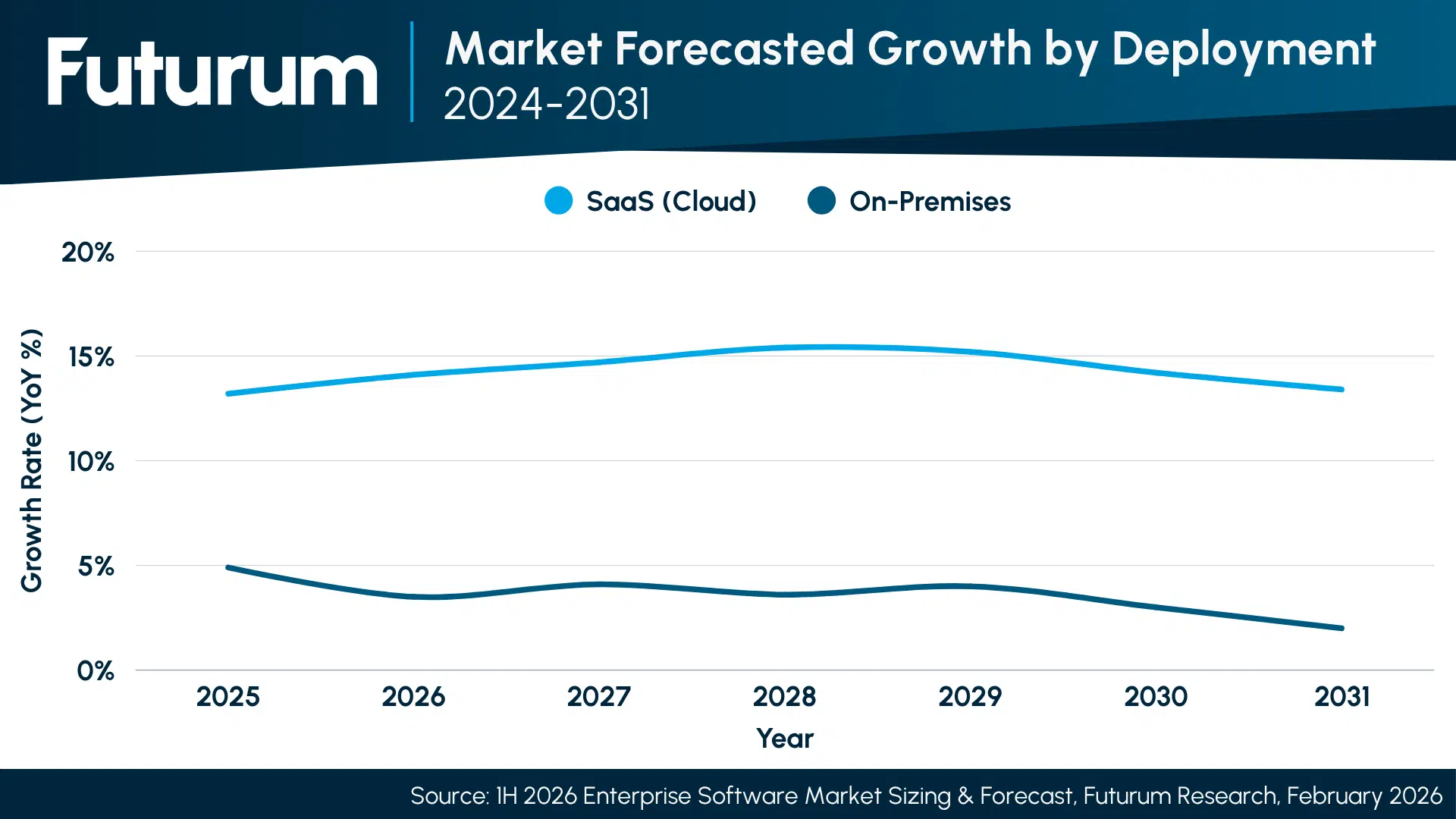

Indeed, the Enterprise Applications market is projected to grow from $370.9B in 2024 to $604.0B by 2031 (7.2% CAGR, Base Case), with SaaS/Cloud deployments commanding 74.7% of the market by 2031, according to Futurum’s 1H 2026 Enterprise Software Market Sizing and Five-Year Forecast. This trajectory reflects enterprises deepening their commitment to SaaS platforms rather than abandoning them, even as AI tools proliferate.

Figure 1: Market Forecasted Growth by Deployment: 2024–2031

Debunking the AI-Developed Enterprise Application Narrative

Developing enterprise applications with AI mistakenly equates code generation with product delivery. AI-assisted outputs are typically just early prototypes, whereas enterprises require the infrastructure, governance, and ecosystem integration of mature platforms. The true value of SaaS lies in the invisible layers below the interface, such as data architecture, compliance frameworks, and operational resilience, which AI coding narratives often overlook.

This is not just a theoretical distinction. In ETR’s SaaS Displacement study, AI was far more likely to accompany vendor additions or partial displacement than to drive outright replacement. In the past 12 months, AI was cited as the replacement type in 67% of add-alongside decisions and 62% of partial replacements, but only 26% of full displacements. That pattern suggests AI is pressuring workflows and seats before it eliminates core platforms.

Nowhere is that more obvious than in data management and orchestration. Enterprise platforms such as Adobe, Google, HubSpot, Microsoft, Salesforce, SAP, ServiceNow, Zendesk, Zoho, and others have invested billions in building unified customer data models that can resolve identities across channels, deduplicate records, manage consent, and preserve data quality across millions of records and countless touchpoints.

Although a CRM built via AI tools might store contacts and opportunities, it is not the same as maintaining a continuously governed, real-time customer identity graph across marketing, sales, service, and analytics. Nor is it the same as integrating that system with ERP, HR, e-commerce, payments, or supply chain platforms through prebuilt connectors and orchestration layers. The enterprise applications market spans numerous interdependent categories, and the value of SaaS often lies less in any one application than in the connective tissue between them. An AI-generated app starts from zero on every one of those connection points.

ETR’s CRM Observatory data reinforces this point. Microsoft Dynamics led or tied for first on five of ten product strength attributes, including 91% for technical expertise and 84% for ecosystem integration, while Salesforce posted the highest difficulty-to-replace score at 68%. These results point to platform depth, available expertise, and ecosystem integration as sources of defensibility that are not easily recreated by generating a new application interface.

Managing Intra-Organizational Workflows and Data

That challenge becomes even more consequential when workflows cross functional boundaries. Modern enterprises do not operate through isolated apps; they operate through chains of processes. A marketing lead becomes a sales opportunity, which becomes a customer account, which triggers onboarding, billing, forecasting, service workflows, and analytics updates. Each step must account for role-based access, approvals, exception handling, SLAs, and auditability.

Enterprise SaaS vendors have spent decades building the workflow engines and operational logic that support this complexity. Their value is not just that they provide a sales, marketing, or service module; it is that they have already built the machinery that lets those modules function as part of a larger enterprise operating model. That is also why buyers continue to prioritize flexibility, AI capabilities, and adaptability over raw cost alone: they know that workflow complexity is expensive to recreate from scratch, even if the code itself can now be generated more quickly.

The same logic applies, perhaps even more urgently, to agentic AI. There is a major difference between generating an AI agent and safely deploying one in an enterprise environment. Agentic AI presents an architectural challenge that requires orchestration, permissions, human oversight, escalation paths, logging, policy controls, and governance. Enterprises are already deeply concerned about loss of human control, security vulnerabilities, unpredictable agent behavior, integration complexity, and regulatory exposure. Those are not coding problems. They are platform and governance problems.

Vendors such as Salesforce, Microsoft, and ServiceNow are not merely introducing AI agents; rather, they are building the infrastructure needed to monitor, constrain, and operationalize them. AI-generated applications and agents created outside those systems may be technically functional, but by default, they lack the governance guardrails that enterprises need to trust them. Even with major platform support, most organizations are still early in their maturity journey around governed AI adoption. Building without that foundation only magnifies the risk.

The ETR SaaS Displacement category-level data also shows that AI disruption varies by workflow domain. Data & Analytics/BI is one of the few categories where AI assistants outpace traditional SaaS swaps, at 32% in both the past and next 12 months. By contrast, CRM/Sales Technology remains more stable, with two-thirds reporting no meaningful vendor change, and IT Operations/ITSM shows rising stability even as respondents describe active AI deployment inside existing platforms.

The Experience and Expertise Gap

Enterprise SaaS also delivers something less visible but equally valuable: accumulated operational knowledge. Over the last twenty years, major software vendors have encoded best-practice workflows, default configurations, process logic, and industry benchmarks into their products. That includes not just horizontal workflows such as pipeline management, campaign orchestration, service routing, financial close, and HR lifecycle management, but also vertical workflows that are deeply industry-specific.

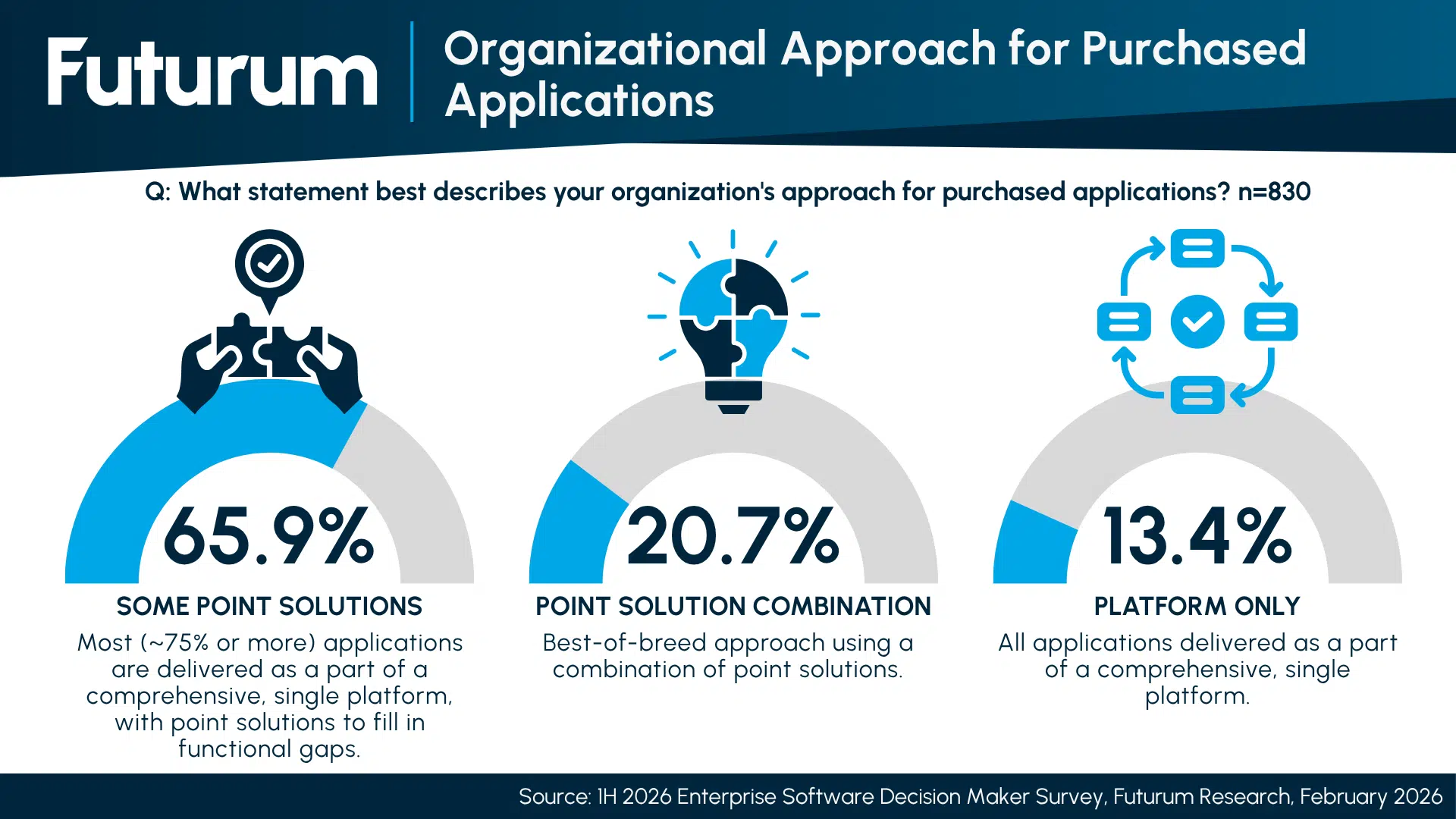

It is hardly surprising that enterprise buyers have and continue to favor a SaaS-based, platform-first approach to building out their application stacks. Futurum’s 1H 2026 Enterprise Software Decision Makers Survey found that 65.9% of enterprise buyers currently follow a platform-first approach supplemented by point solutions, and 41.0% are actively consolidating their application stacks, signaling that the market is moving toward fewer, more integrated platforms, not more homegrown tools.

Figure 2: Organizational Approach for Purchased Applications (n=830)

Additional research conducted directly with IT decision makers provides further support for this argument. ETR’s February 2026 SaaS Displacement study surveyed 152 IT decision makers across 12 enterprise software categories and found that AI-driven SaaS displacement is not yet a broad enterprise reality. Most IT leaders report no meaningful vendor strategy change, typically 50% to 70% by category, and traditional SaaS-to-SaaS switching remains the primary driver of change in 10 of 12 categories.

Furthermore, building a HIPAA-compliant patient engagement workflow, a SOX-aware finance process, or a regulated banking onboarding journey is far more complex and challenging using AI to build a generic CRM. Indeed, the value of software lies not just in what it does, but in what it already knows about the requirements of the environment it operates within. That domain expertise is difficult to commoditize, and it is one reason industry-specific SaaS vendors continue to command premium relevance.

Then there is the hidden operational burden of ‘owning’ software. SaaS subscriptions are often criticized for their recurring cost, but what they really buy is the offloading of complexity, skills, and effort. Vendors absorb the responsibility for patching, performance optimization, uptime, compliance updates, infrastructure scaling, and product evolution. They push major releases, deliver new features, and keep pace with changing security and regulatory demands.

A homegrown or AI-generated application may be faster to create, but it also creates a long-term maintenance obligation. Every integration, every dependency, every security vulnerability, and every changing business requirement becomes the enterprise’s problem to manage. That is one reason cloud and SaaS deployment models continue to gain share: organizations are not voting to bring more software burden in-house. They are increasingly paying vendors to absorb it.

Cost pressure does not invalidate the platform model; it changes the way platforms must prove value. ETR’s write-in analysis found that cost, cloud migration, and platform consolidation often sit alongside AI as drivers of change. In other words, enterprises are not simply choosing between AI and SaaS; they are trying to fund AI adoption by rationalizing legacy spend, reducing tool sprawl, and moving more workloads to cloud-native platforms.

AI-Native’s Role in the Enterprise Stack

That does not mean AI-native development tools are unimportant. It means their greatest value lies somewhere more strategic than replacing enterprise SaaS outright. The real opportunity is in extension, not substitution. AI-assisted development is exceptionally useful for ad hoc reporting, custom dashboards, lightweight role-specific interfaces, fast integrations, and proof-of-concept development. These are exactly the areas where enterprise platforms often feel too rigid, too slow, or too expensive to customize through traditional methods.

A sales leader who needs a custom pipeline analysis, a field technician who needs a simplified mobile interface, or an IT team that needs a custom connector between SAP and Salesforce may get enormous value from AI-native tools. In those cases, AI is not replacing the enterprise platform. It is making the platform more adaptable, more responsive, and more useful to the people who rely on it.

This is where third-party AI can create disproportionate value: not by rebuilding the core system, but by making it easier to personalize, automate, and operationalize the work that surrounds it. In CRM, for example, ETR respondent commentary included examples of agentic CRM handling 80% of lead qualification and bespoke LLM-powered user experiences built after dissatisfaction with an incumbent. Those examples point to workflow substitution and targeted augmentation, not necessarily wholesale platform displacement.

Indeed, in the ETR CRM/Sales Technology data cut, 67% of respondents reported no meaningful vendor strategy change in the past 12 months, and 66% expected no meaningful change over the next 12 months. Among those making changes, traditional SaaS vendor swaps were still the leading change type at 19%, while AI assistants/agents grew modestly to 14%.

The same CRM market data also illustrates why core platforms remain resilient. ETR’s May 2026 CRM Observatory, based on 306 IT decision makers, identifies Salesforce, Microsoft, ServiceNow, and HubSpot as the leading CRM cluster by spending and utilization metrics, with ServiceNow posting the highest spending Net Score at 58% and Salesforce, Microsoft, and HubSpot clustered at 52% to 53%.

The Hierarchy for Building, Buying, or Extending Enterprise Applications

The data support an adoption of a more grounded strategic framework for enterprise buyers: build, buy, or extend. Core enterprise workflows, which encompass the systems that are mission-critical, cross-functional, compliance-sensitive, and deeply embedded in business operations, should generally be bought as enterprise-grade SaaS. Departmental customizations, workflow extensions, role-specific interfaces, and connective integrations are often best handled by extending those SaaS platforms through APIs and AI-native tools.

Furthermore, leveraging Model Context Protocol (MCP) servers and native APIs to enable the so-called headless access to core data is often best executed by SaaS platforms with built-in governance and security. Short-lived utilities, one-time scripts, migration helpers, or prototypes are where vibe coding truly shines. That is the right hierarchy.

The mistake is not using AI to build applications; it is using AI to build the wrong applications. The further a system moves toward core process, regulated data, or organizational dependency, the more dangerous it becomes to confuse ‘working code’ with ‘production-ready platform’.

The broader market context reinforces this conclusion. If AI-assisted development were truly poised to replace enterprise SaaS at scale, the enterprise applications market would be shrinking, SaaS deployment would be in retreat, and displacement data would show AI-led replacement outpacing traditional vendor swaps across most categories.

However, the opposite picture is emerging. The enterprise applications market continues to grow, SaaS continues to gain share, platform consolidation remains a dominant buyer strategy, and Futurum and ETR data illustrate that AI is most often augmenting or reshaping existing software estates rather than eliminating them. Enterprises are not preparing to fragment their software estates into dozens of AI-generated internal tools. They are trying to reduce complexity, not multiply it. In practice, that means fewer core platforms with deeper adoption, and more demand for flexible ways to extend them.

Conclusion: Code Generation Is Not Product Delivery

The strategic takeaway is straightforward. Enterprises should not confuse code generation with product delivery, and SaaS vendors should not respond to AI-native development by defending yesterday’s application boundaries. AI can dramatically compress the time required to prototype, customize, and connect systems, and that is a meaningful shift. But enterprise SaaS still derives its value from the operational maturity, governance, integration, data quality, ecosystem depth, and workflow intelligence that sit beneath the interface.

The organizations that win in this environment will not be the ones that try to rebuild Salesforce, SAP, ServiceNow, Microsoft, or Adobe from scratch with prompts. They will be the ones that use third-party AI and AI-native tools to make those platforms more adaptable, more connected, and more aligned with the realities of how their businesses actually work.

What to Watch

- Whether enterprises actually cut core SaaS spend, or simply redirect custom development budgets. The key question is whether AI-native tools meaningfully replace major SaaS commitments, or mostly get used for extensions, prototypes, and departmental utilities.

- How quickly platform vendors productize ‘AI-assisted extensibility’. Watch whether major SaaS vendors make it dramatically easier to build custom apps, interfaces, workflows, and connectors inside their ecosystems rather than outside them.

- The emergence of agent governance as a formal buying requirement. Expect more scrutiny around agent permissions, audit trails, model behavior controls, and compliance readiness as enterprises move from experimentation to production AI deployment.

- A widening divide between core systems and edge apps. Over the next year, the market may increasingly separate into two layers: durable systems of record that remain bought from established vendors, and a fast-growing edge layer of AI-generated tools, utilities, and interfaces built around them.

- Which categories become early proof points for AI-led replacement. Data & Analytics/BI and Developer Tools/DevOps show stronger AI-led change than most categories, while CRM and ITSM remain comparatively insulated. Buyers and vendors should avoid treating AI disruption as uniform across the software stack.

- Whether AI pressure shows up first as seat compression rather than platform displacement. ETR’s data suggests the near-term risk for many SaaS vendors is workflow substitution and wallet-share pressure, not wholesale category replacement.

Source Notes

- Futurum’s 1H 2026 Enterprise Software Market Sizing and Five-Year Forecast

- Futurum, 1H 2026 Enterprise Software Decision Makers Survey

- ETR, SaaS Displacement Drill Down, February 2026. Survey of 152 IT decision makers across 12 enterprise software categories, including category-level analyses of CRM/Sales Technology, Customer Support/Contact Center, Data & Analytics/BI, IT Operations/ITSM, and cross-category commentary.

- ETR, Observatory for Customer Relationship Management (CRM), May 2026. Survey of 306 IT decision makers evaluating spending trends, product strength, ROI, NPS, usage, and expected length of use across 20 CRM vendors.

Other Insights from Futurum

Enterprise AI ROI Shifts as Agentic Priorities Surge

Is SaaS Facing a Threat from AI Automation?

Code Generation and Process Automation Set to Lead AI Use Case Revenue

Disclosure: Futurum is a research and advisory firm that engages or has engaged in research, analysis, and advisory services with many technology companies, including those mentioned in this article. The author does not hold any equity positions with any company mentioned in this article.

Analysis and opinions expressed herein are specific to the analyst individually and data and other information that might have been provided for validation, not those of Futurum as a whole.

Read the full Futurum Group Disclosure.

Author Information

Keith Kirkpatrick is VP & Research Director, Enterprise Software & Digital Workflows for The Futurum Group. Keith has over 25 years of experience in research, marketing, and consulting-based fields.

He has authored in-depth reports and market forecast studies covering artificial intelligence, biometrics, data analytics, robotics, high performance computing, and quantum computing, with a specific focus on the use of these technologies within large enterprise organizations and SMBs. He has also established strong working relationships with the international technology vendor community and is a frequent speaker at industry conferences and events.

In his career as a financial and technology journalist he has written for national and trade publications, including BusinessWeek, CNBC.com, Investment Dealers’ Digest, The Red Herring, The Communications of the ACM, and Mobile Computing & Communications, among others.

He is a member of the Association of Independent Information Professionals (AIIP).

Keith holds dual Bachelor of Arts degrees in Magazine Journalism and Sociology from Syracuse University.