The News: Microsoft shares barely moved in extended trading on Tuesday after the company reported fiscal first-quarter results that were better than analysts had expected.

Here’s how the company did:

- Earnings: $1.82 per share, adjusted, vs. $1.54 per share as expected by analysts, according to Refinitiv.

- Revenue: $37.15 billion, vs. $35.72 billion as expected by analysts, according to Refinitiv.

Microsoft revenue grew 12% on an annualized basis, down from 13% growth in the prior quarter, according to a statement. Read the full news piece on CNBC.

Analyst Take: Microsoft delivered a robust result in its fiscal Q1, reporting revenue of $37.2B and EPS of $1.82, topping consensus estimates of $35.76B and $1.54.

The company realized impressive double-digit growth in Revenue, Operating Income, Net Income, and EPS across the board, which should add to investors’ confidence despite recent market turbulence and the ongoing impacts of the pandemic and election. Microsoft confirmed that it is clearly a

- Revenue was $37.2 billion and increased 12%

- Operating income was $15.9 billion and increased 25%

- Net income was $13.9 billion and increased 30%

- Diluted earnings per share was $1.82 and increased 32%

In this earnings report, I was closely watching the company’s performance in three major areas. Productivity, Intelligent Cloud, and Personal Devices/Computing. The company had strong results in all three, with Intelligent Cloud and Azure leading the way:

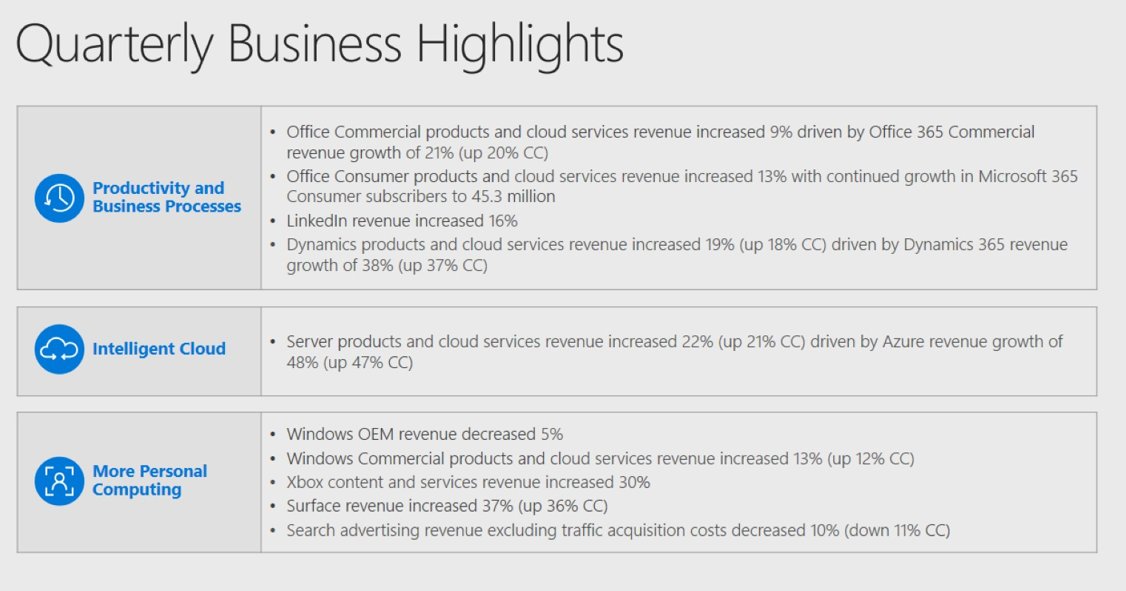

Intelligent cloud and Azure saw strong growth at 20% and 48%, respectively, showing continued strong cloud demand. There seemed to be some question marks around cloud demand, especially following weaker earnings and guidance from cloud ERP leader, SAP. Microsoft’s results showed the company to be un-phased during this quarter.

Speaking of ERP, this fits into Microsoft’s Productivity segment, which saw continued double-digit growth (11%) as demand for Office 365 continues to rise. The area that caught my attention the most though was the growth of Microsoft’s own play in CRM/ERP, its Dynamics, and Dynamics 365 business. With Power Platform gaining momentum and driving greater adoption, as well as traditional Dynamics and Cloud ERP (Dynamics 365) continuing to be big for this category driving 38% growth, some of my early speculations about a tighter race in business productivity seem to be gaining momentum–especially with Salesforce and Microsoft continuing to look like the fiercest of competitors.

The last category that I wanted to track closely was the “More personal” segment, which saw 6% category growth led by big growth in Surface at 37% and Xbox content and services at 30%. I’ve been very impressed with the new product rollout of Surface and watched to see if Microsoft may be poised to displace Apple as the ultra-premium laptop and computing platform. This could become more probable if Apple stumbles at all with its in-house chips that are set to replace Intel. Microsoft has delivered a wide swath of device types, all of which have a premium look and feel, but run Windows, which is much cooler than it used to be. Microsoft variants include Intel, AMD, and Arm chips. I think that was a smart move by Microsoft.

Lastly, I found this quarter to continue Microsoft’s interesting partnerships, including two in the past few weeks. The first is a partnership to drive growth in Industrial via a partnership with Honeywell. The other is an interesting reimagining of CRM with a new vertical focused AI-powered CRM app with Adobe and Tom Seibel’s newest startup C3.ai.

Overall Impressions of Microsoft FY 21 Q1 Earnings

Overall, an excellent quarter for Microsoft. The key is going to be maintaining this strong momentum. As its cloud continues to grow, large numbers can challenge big growth percentages. However, even the pandemic and its lingering effects have attached to digital investment rather than cut spending. This is why I’m optimistic that Microsoft will weather any future setbacks due to the election or pandemic without incident.

Futurum Research provides industry research and analysis. These columns are for educational purposes only and should not be considered in any way investment advice.

Read more analysis from Futurum Research:

IBM Spin-Off Illuminates its Big Cloud Bets and Why Growth is a Must

AMD Double Splash: Announcing Xilinx Deal and Posting Big Q3 Earnings

Microsoft, C3.ai, and Adobe Partner to Reimagine CRM

Image: Microsoft/CNN

Author Information

Daniel is the CEO of The Futurum Group. Living his life at the intersection of people and technology, Daniel works with the world’s largest technology brands exploring Digital Transformation and how it is influencing the enterprise.

From the leading edge of AI to global technology policy, Daniel makes the connections between business, people and tech that are required for companies to benefit most from their technology investments. Daniel is a top 5 globally ranked industry analyst and his ideas are regularly cited or shared in television appearances by CNBC, Bloomberg, Wall Street Journal and hundreds of other sites around the world.

A 7x Best-Selling Author including his most recent book “Human/Machine.” Daniel is also a Forbes and MarketWatch (Dow Jones) contributor.

An MBA and Former Graduate Adjunct Faculty, Daniel is an Austin Texas transplant after 40 years in Chicago. His speaking takes him around the world each year as he shares his vision of the role technology will play in our future.