Analyst: Brendan Burke

Publication Date: June 23, 2026

Document #: AINBB202606

Recent federal and private investments totaling $4.6 billion are establishing a dedicated U.S. quantum foundry infrastructure modeled after the successful TSMC playbook. While these foundries are essential for scaling qubit production, this report highlights that the true determinant of market leadership will be securing capacity within the downstream cryogenic and packaging supply chain.

What You Need to Know

- On May 21, 2026, the U.S. Department of Commerce signed letters of intent totaling $2.0 billion in CHIPS Act incentives with nine quantum companies, taking a minority equity stake in each.

- Two awards fund dedicated quantum foundries. IBM received $1 billion to launch Anderon, a standalone 300mm superconducting-wafer fab in Albany, New York. On June 2, IBM separately committed more than $10 billion over five years to its quantum roadmap, targeting the first large-scale fault-tolerant system, Starling, in 2029.

- GlobalFoundries received $375 million to build Quantum Technology Solutions, a foundry spanning superconducting, trapped-ion, photonic, topological, and silicon-spin qubits, extending its existing volume-manufacturing work with PsiQuantum.

- Seven awards of $38 million to $100 million each fund qubit developers, including Atom Computing, Diraq, D-Wave, Infleqtion, PsiQuantum, Quantinuum, and Rigetti, each aimed at a specific engineering challenge.

- The money lands in an industry that is already forming. IonQ is acquiring foundry SkyWater for about $1.8 billion. SkyWater also fabricates qubits for D-Wave and control chips for QuamCore, among nine quantum clients. Rigetti runs the only U.S.-owned superconducting quantum fab in commercial operation. QuantWare presents a European alternative with 3D routing technology.

Recommendations

For vendors competing in the new American quantum foundry industry, three priorities stand out:

- Treat Fabrication Capacity as a Core Asset: Reproducible, high-yield manufacturing at 300mm and 200mm scales now decides which qubit designs reach the market. Market leadership will derive from process design kits, in-line testing, and reliable iteration.

- Map Quantum Breakthroughs to Foundry Capacity to Forecast Commercial Impact: Anderon focuses on superconducting depth, GlobalFoundries spans five modalities, Rigetti owns the full stack, and IonQ and SkyWater pursue vertical integration of trapped-ion quantum processing units (QPUs). Align roadmaps and packaging choices to one of these models.

- Reserve the Cryogenic and Packaging Chain Early: Dilution refrigerators, helium-3, and advanced packaging now set delivery timelines, so qubit developers should lock in cryo-cabinet and packaging capacity alongside wafer slots, the way fabless logic firms secured TSMC capacity in the 1990s.

Analysis

For a decade, quantum progress was measured in qubit counts and coherence times. Three announcements in Q2 2026 redirect attention to manufacturing:

- On May 8, SkyWater Technology stockholders approved a $1.8 billion acquisition by IonQ.

- On May 21, the U.S. Department of Commerce committed $2.0 billion to nine quantum companies and took equity in each. Out of this, $1.8 billion was allocated to companies building a Quantum Foundry or partnering with one (see below).

- On June 2, IBM committed more than $10 billion over five years to its quantum roadmap, spanning research, capital expenditure, and manufacturing scaling, on the path to the first large-scale fault-tolerant system in 2029. The company invested an incremental $1 billion into its Quantum Foundry called Anderon after the CHIPS Act award.

Together, these commitments total $4.6 billion, and they point to one idea: the next TSMC can be a quantum foundry. The history of TSMC shows what that idea costs, and it also reveals the link in the supply chain that will decide the race. The fab earns the headlines. The cryogenic and packaging chain will become the new bottleneck.

What a Quantum Foundry Now Means

Through 2024, ‘quantum foundries’ largely referred to any academic lab capable of fabricating a handful of qubit wafers for research purposes. The 2026 expectation is a true wafer fab that produces quantum-grade devices at volume for multiple vendors, with the process design kits, in-line characterization, and yield discipline that logic-chip customers expect. The industry is adopting the fabless-and-foundry structure that reshaped classical semiconductors in the 1990s. Anderon describes itself as an anchor for a national ecosystem serving multiple quantum hardware vendors, language drawn straight from the TSMC model.

The TSMC Playbook

TSMC became the most strategic company in semiconductors because Taiwan funded it as national infrastructure. At the company’s founding in 1987, the Taiwanese government supplied 48.3% of the startup capital through its National Development Fund, recruited Morris Chang from the U.S. semiconductor industry to run it, and asked the island’s wealthiest families to take another fifth of the equity. Philips contributed technology transfer and intellectual property for a 27.6% stake.

Public capital, a foreign technology partner, and a pure-play foundry model combined to turn a modest NT$1.3 billion start, about $45 million at the time, into the foundry that now produces most of the world’s advanced logic. The 2026 quantum commitments echo that structure. The Department of Commerce provides public capital and takes equity, as Taiwan’s development fund did. IBM supplies the technology base for Anderon, as Philips did for TSMC. The United States is running the TSMC playbook on quantum, four decades later and on its own soil.

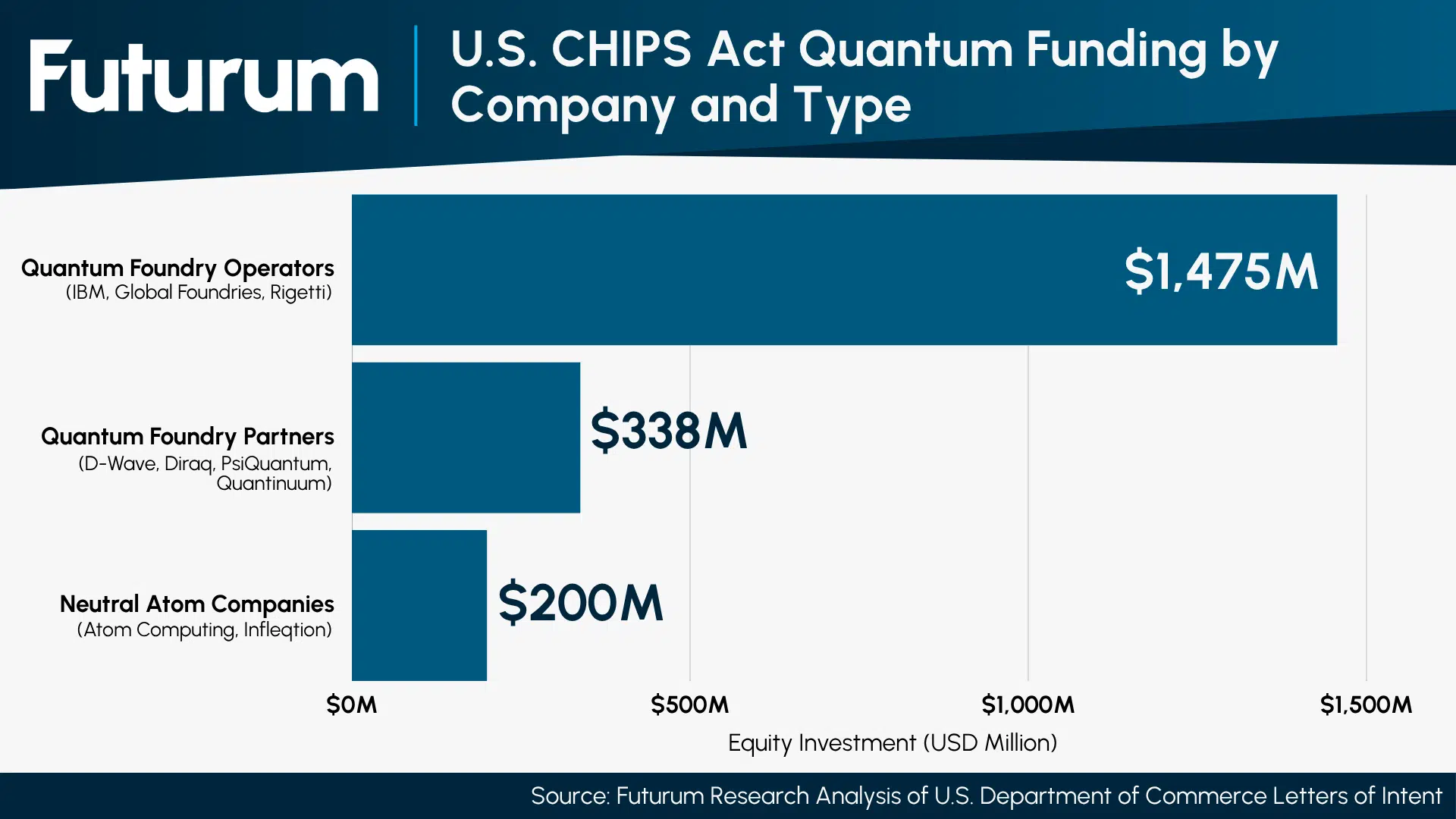

Of the $2.013 billion in CHIPS Act quantum incentives, $1.475 billion went directly to quantum foundry operators: $1 billion to IBM for its Anderon wafer foundry, $375 million to GlobalFoundries for Quantum Technology Solutions, and $100 million to Rigetti, which runs its own Fab-1. An additional $338 million went to companies actively partnering with quantum foundries rather than owning one, namely D-Wave (fabricating at SkyWater), PsiQuantum (at GlobalFoundries), Quantinuum (ion traps at Honeywell and Infineon), and Diraq (silicon-spin devices at imec and GlobalFoundries). The remaining roughly $200 million went to the two neutral-atom companies, Atom Computing and Infleqtion, which do not require a wafer foundry because they manufacture custom optical traps and hold their qubits as individual atoms rather than fabricated devices.

Taken together, more than 90% of the funding flows to firms that either operate or feed a quantum foundry, which shows the program’s intent to incubate a domestic manufacturing base for a new economy that TSMC has not yet addressed.

Figure 1: U.S. CHIPS Act Quantum Funding by Company and Type

Source: Futurum Research Analysis of U.S. Department of Commerce Letters of Intent

What Production-Scale Yield Requires

Reaching production-scale yield depends on a chain of capabilities that reaches well past the wafer. Five links carry the load:

- Cryogenic Test Throughput: Quantum devices reach their working state near absolute zero, so fabs validate them on wafer-scale cryogenic testers. Throughput on these testers governs how fast a foundry screens wafers and feeds yield data back into the process.

- Advanced Packaging: Scaling to the logical qubit targets set out by quantum leaders requires heterogeneous integration. Builders place qubit arrays on a die, connect dies through 2.5D interposers and through-silicon vias, and network the modules together. Packaging capacity sets the pace toward systems with hundreds of thousands of qubits.

- Dilution Refrigerators and Cryo-Cabinets: Every superconducting system and many spin-qubit systems operate inside a dilution refrigerator. Three suppliers serve the world, led by Bluefors, with Oxford Instruments and Janis Research behind it, and lead times of six to nine months collide with hardware cycles of twelve to eighteen months.

- Cryo-CMOS Control Electronics: Scaling qubit counts depends on moving control functions onto the silicon beside the qubits. IonQ describes its path to a 10,000-qubit chip through active CMOS design, where foundry partner SkyWater places control directly on the chip.

- Helium-3 and Interconnect Supply: Dilution refrigerators cool with helium-3, which makes up 0.0001% of all helium and sells for $1,900 to $2,600 per liter, sourced from tritium decay in nuclear weapons stockpiles. Cryogenic interconnects and microwave wiring draw on the same thin supply base.

The Binding Constraint Is the Cryo-and-Package Chain

The fab attracts the capital and the headlines, yet the binding constraint sits downstream, in the cryogenic and packaging chain. A foundry can pattern thousands of wafers yet finished quantum processing units (QPUs) are limited by dilution refrigerators volume and packaging lines capacity. Dilution refrigerators rank as the single most acute bottleneck for superconducting and several spin-qubit systems, and helium-3 supply caps how many of those refrigerators run at once.

This reframes the $13.8 billion in recent investment announcements. The largest checks fund wafer fabs, while the scarcer assets sit in Syracuse, New York, where Bluefors builds refrigerators, and in the federal helium-3 stockpile. The company that secures cryogenic test throughput, packaging capacity, and a helium-3 supply will out-ship the company that owns the cleanest fab alone. Capacity at the fab is necessary. Capacity in the cryo-and-package chain will be decisive.

How the Capital Influx Reshapes the Existing Landscape

Federal money landed on an industry that private capital and defense contracts already built. The CHIPS awards accelerate complementary foundry models and lock four of five inside the United States.

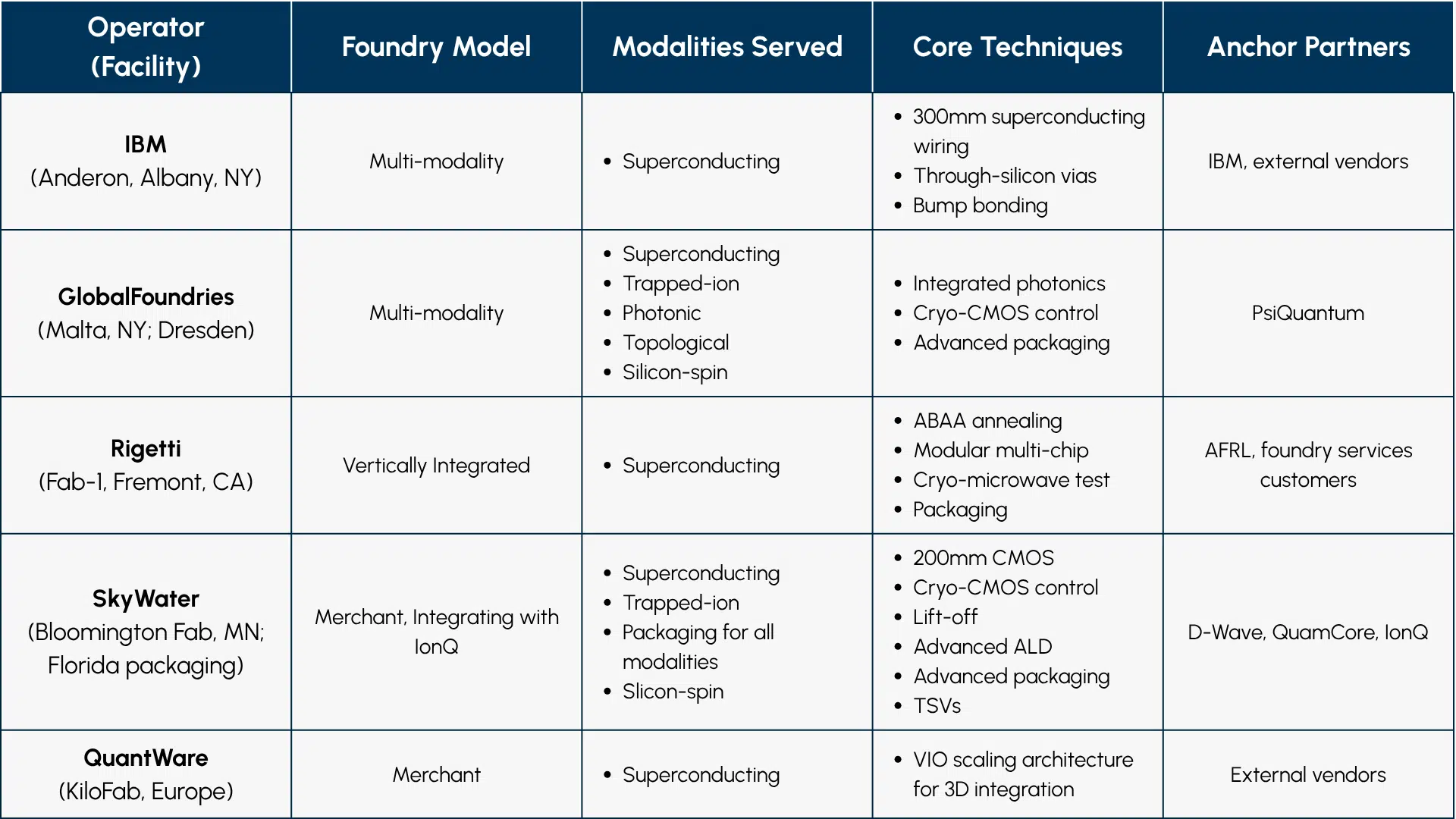

- Anderon will pursue IBM’s superconducting model from today’s commercial systems toward the fault-tolerant Starling machine in 2029. IBM is building 300mm superconducting wiring, through-silicon vias, and bump bonding, and offering that capacity to outside vendors from Albany. It enters as the largest single bet in the field.

- GlobalFoundries carries the multi-modality model. Its $375 million extends a commercial 300mm operation that already fabricates PsiQuantum’s Q1 silicon-photonic chips in Malta, New York and cryogenic control electronics in Dresden, Germany. The spin-out Quantum Technology Solutions will serve superconducting, trapped-ion, photonic, topological, and silicon-spin customers, specializing in integrated photonics, cryo-CMOS control chips, and advanced packaging.

- Rigetti initiated the vertically integrated model. Its Fab-1 in Fremont, California, established in 2017, remains the only U.S.-owned superconducting quantum fab in commercial operation, covering design, fabrication, cryo-microwave test, and packaging under one roof. Rigetti’s proprietary ABAA (alternating-bias-assisted annealing) process and modular multi-chip architecture target qubit fidelity and scale, and its $100 million CHIPS Act award funds miniaturized readout electronics and next-generation cryostats. Rigetti also sells foundry services to outside customers, including a five-year agreement with the Air Force Research Laboratory.

- SkyWater operates under the merchant foundry model and is now being acquired by IonQ in a pending $1.8 billion transaction that SkyWater stockholders approved on May 8, 2026. This DMEA-accredited Trusted foundry in Bloomington, Minnesota, fabricates D-Wave’s annealing qubits and co-develops single-flux-quantum (SFQ) control chips with QuamCore, and its 200mm CMOS process anchors IonQ’s path to a 10,000-qubit chip by placing control functions directly on silicon. The deal converts SkyWater’s Minnesota, Florida, and Texas sites into Regional Quantum Production Hubs and gives IonQ a domestic, trusted supply chain, with advanced packaging concentrated in Florida.

- QuantWare is the world’s largest commercial QPU supplier by volume and specializes in 3D integration for vertical signal routing. The company recently raised $178 million in a round co-led by Intel Capital, indicating the strategic nature of Quantum Foundry to fabrication incumbents. Its VIO (Vertical I/O) architecture stacks quantum chiplets and interposer layers to deliver control signals vertically into the qubits rather than fanning wiring across a flat die, scaling to 10,000-qubit processors. To meet fabless customer demand, it is building KiloFab at its Delft, Netherlands headquarters, which it calls the world’s largest dedicated quantum foundry that raises production capacity roughly 20x, positioning QuantWare as Europe’s merchant foundry answer to the U.S. capacity buildout.

Figure 2 maps these four models, the modalities each serves, and the techniques each brings to the market.

Figure 2: The American Quantum Foundry Landscape After the 2026 Investments

Source: Futurum Group analysis of company disclosures and U.S. Department of Commerce filings, June 2026

A New Strategic Industry

Taiwan turned wafer manufacturing into national leverage, and the country that hosted the leading foundry gained influence over the entire semiconductor supply chain. The United States now holds an early lead in quantum fabrication through Rigetti, SkyWater, GlobalFoundries, and IBM, and the recent influx of $13.8 billion of public and private capital converts that lead into national infrastructure. QuantWare presents a European hope. China is building superconducting quantum processors domestically, led by USTC’s academic Zuchongzhi line and Origin Quantum’s commercial Wukong machines in Hefei, using standard mature-node lithography that sidesteps EUV export controls. In response to those controls, it is vertically integrating the entire supply chain, including domestically produced dilution refrigerators and control electronics, prioritizing self-sufficiency over the merchant-foundry model the U.S. is pursuing. The challenger that manufactures quantum chips at scale will hold the leverage over quantum computing that TSMC holds over logic. The result will turn on whoever also controls the cryogenic and packaging chain that turns wafers into working machines.

What to Watch

Four variables will decide whether more than $14 billion in commitments compounds into durable advantage.

- Cryogenic and Helium-3 Supply: Dilution refrigerator lead times, Bluefors capacity in Syracuse, and federal helium-3 allocation will set the ceiling on shipments.

- Yield and Customer Wins: The five early foundries will prove their value through published process design kits, defect-density data, and external customer announcements across 2026 and 2027.

- Modality Leadership: A decisive scaling or error-correction result in one modality will reward the foundries aligned to it. Superconducting maturity favors Anderon and Rigetti today, while a photonic, neutral-atom, or trapped-ion breakthrough rewards the breadth of GlobalFoundries and SkyWater. Advancements in optical control technologies may reduce the value of the foundry model overall.

- Vertical Integration versus Merchant Capacity: The IonQ and SkyWater combination tests whether owning a foundry beats buying capacity, and its results will guide how D-Wave, Quantinuum, and others structure their own supply chains.

For the underlying announcements, see IBM’s $10 billion quantum commitment and the Department of Commerce letters of intent.

Disclosure: Futurum is a research and advisory firm that engages or has engaged in research, analysis, and advisory services with many technology companies, including those mentioned in this article. The author does not hold any equity positions with any company mentioned in this article.

Analysis and opinions expressed herein are specific to the analyst individually and data and other information that might have been provided for validation, not those of Futurum as a whole.

Other Insights from Futurum

IBM Maps a $10 Billion Path to Fault-Tolerant Quantum Computing

$2 Billion CHIPS Act Investment in Quantum Bets on IBM’s 300mm Superconducting Silicon

SkyWater’s CEO Letter Redefines the US Foundry Model

Author Information

Brendan is Research Director, Semiconductors, Supply Chain, and Emerging Tech. He advises clients on strategic initiatives and leads the Futurum Semiconductors Practice. He is an experienced tech industry analyst who has guided tech leaders in identifying market opportunities spanning edge processors, generative AI applications, and hyperscale data centers.

Before joining Futurum, Brendan consulted with global AI leaders and served as a Senior Analyst in Emerging Technology Research at PitchBook. At PitchBook, he developed market intelligence tools for AI, highlighted by one of the industry’s most comprehensive AI semiconductor market landscapes encompassing both public and private companies. He has advised Fortune 100 tech giants, growth-stage innovators, global investors, and leading market research firms. Before PitchBook, he led research teams in tech investment banking and market research.

Brendan is based in Seattle, Washington. He has a Bachelor of Arts Degree from Amherst College.