Analyst(s): Tiffani Bova, Alex Smith

Publication Date: April 17, 2026

AI is collapsing the GSI consulting pyramid, ushering in the Orchestration Era. Vendors now must shift to outcome-based partnerships.

The Big Picture

The Global System Integrator (GSI) landscape has undergone a more fundamental structural shift in the past 18 months than it did in the previous decade. AI agents now execute the analytical workflows that once required armies of entry-level consultants. The consulting pyramid, the leverage model that generated margin for three decades, has been automated at its base. The firms that recognized this earliest have replaced it with what Futurum defines as a Lab structure: smaller, technically elite teams deploying proprietary AI-led frameworks instead of person-hours.

The commercial value of enterprise AI is no longer locked inside model capabilities or platform features. It is determined entirely by the quality of delivery execution. Futurum Research defines this inflection point as the Orchestration Era. The vendors still rewarding headcount, services-attached revenue, and billable hours are subsidizing a model that their best partners already walked away from.

Key Findings

The consulting pyramid has collapsed: Accenture, Deloitte, KPMG, and a growing cohort of Frontier Partners have rebuilt their operating models around proprietary IP, agentic platforms, and outcome-based delivery. The shift from Pyramid to Lab is not a future prediction. It is the current operating reality for the most capable integrators.

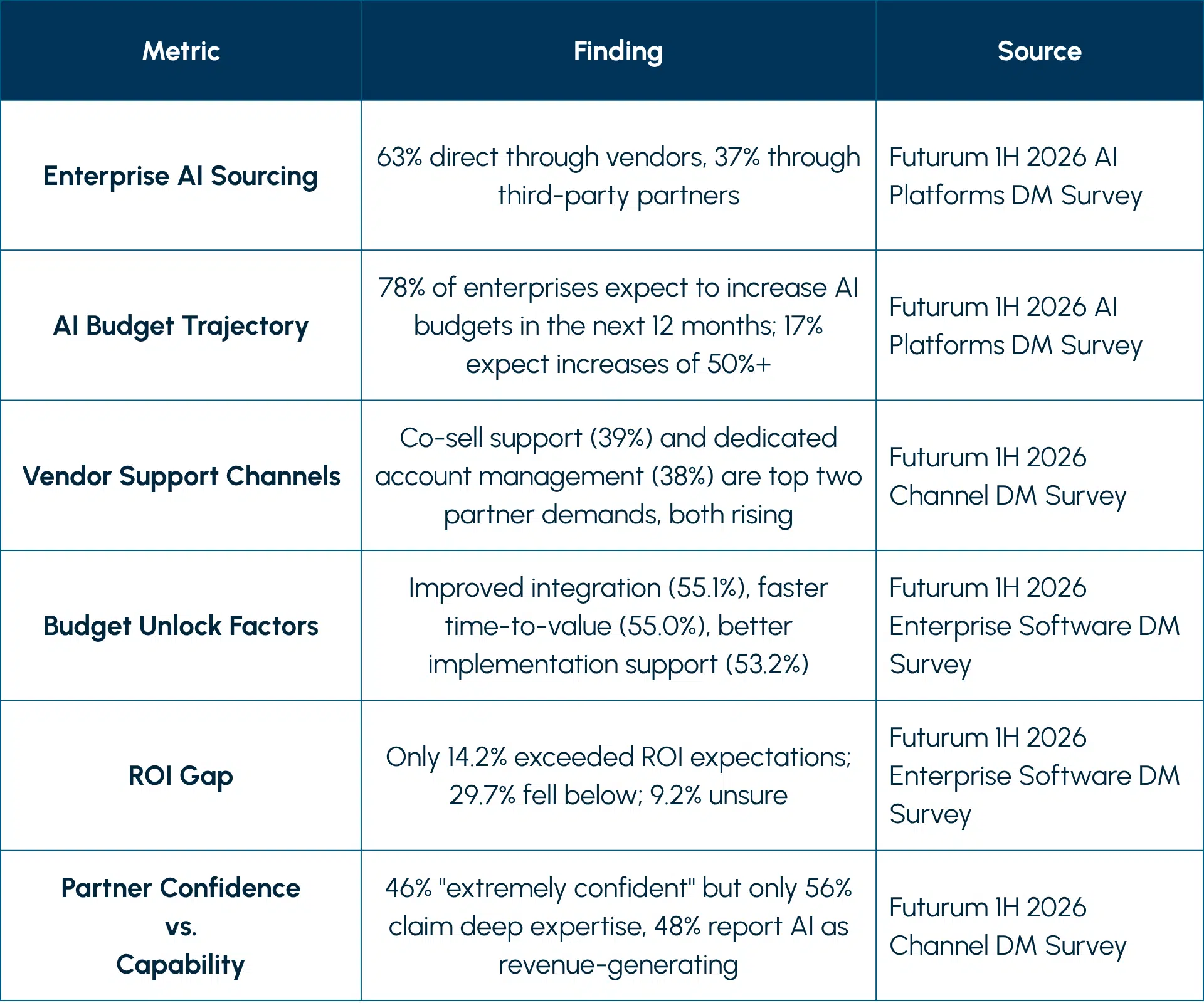

Revenue models are inverting: Frontier Partners go-to-market with flat-fee engagements anchored to measurable business transformation. In Futurum’s 1H 2026 Enterprise Software Decision Maker Survey of 830 executives, 38% indicated that SaaS vendors are missing the mark on competency, specific needs, implementation timeframes, and pricing terms. Only 14.2% of respondents reported ROI exceeding expectations for recent software purchases, while 29.7% reported ROI below expectations. That gap between vendor promises and delivery outcomes is the door Frontier Partners are walking through.

M&A tells you where each GSI is heading: Accenture acquired Faculty and appointed its CEO as Accenture’s CTO. Deloitte acquired Martian and OpTeamizer. KPMG acquired PrivateBlok and Metaphor. EY invested in Covarity and Reveal HealthTech. The pattern is the same across all four: buy the IP, buy the talent, buy the repeatable deployment patterns. Building later is no longer viable.

The alliance matrix is being redrawn: Anthropic, NVIDIA, OpenAI, and Palantir are establishing their own alliance ecosystems. Frontier Partners are gravitating toward these AI pioneers first, rather than legacy vendors that offer AI as one feature among many. The Accenture-Anthropic Business Group, training 30,000 professionals on Claude, signals where strategic partnerships are heading.

Partner confidence exceeds partner capability: Among channel partners, 46% describe themselves as “extremely confident” in their ability to succeed in an AI-transformed market. But only 56% claim deep AI expertise, only 51% have built solutions using LLMs in-house, and only 48% report AI as a revenue-generating business line.

What the Data Says

Recommendations for Vendors

Audit your GSI tier structure against 2026 delivery capabilities now: If your partner program still measures success in services-attached revenue, headcount deployment, or billable hours, you are rewarding firms that are falling behind. Partners want access to your engineers and your deals. Not your courseware.

Create a dedicated Frontier Partner track: Volume-based incentives and product training are not enough for partners that possess their own AI IP, specialized R&D labs, and agentic workflows. Firms such as Decagon, Thinking Machines Lab, Agathon AI, and Tribe AI represent this emerging partner class. Competition to align with them is already underway.

Redesign partner success metrics around customer outcomes: When your best GSI partners sell outcomes instead of hours, tracking services revenue as a proxy for partnership health is a lag indicator at best. If your vendor-defined KPIs do not align with how Frontier Partners measures its own success, it will build without you.

What to Watch

- The M&A frenzy will accelerate: Big Four and Tier 1 integrators will continue acquiring mid-sized AI labs with specialized industry knowledge. Following the Faculty blueprint, this cycle’s acquisitions are about buying capability that cannot be recruited fast enough.

- AI and agentic marketplaces will reshape partner discovery: Salesforce AgentExchange, AWS Marketplace, Google Cloud Marketplace, and Microsoft Marketplace are becoming the primary hubs for discovering, deploying, and monetizing agentic solutions. Anthropic recently launched its own Marketplace. The distribution layer for AI capability is forming now.

- The 63/37 direct-vs-partner sourcing split will shift: As agentic complexity increases and enterprises demand integrated orchestration, the share of AI solutions sourced through partners will grow. The partners who control the orchestration layer will control the customer relationship.

The full report, “The Orchestration Era: Why Your GSI Program Is Already Behind,” is available via subscription to Futurum Intelligence’s Ecosystems, Channels & Marketplaces Practice IQ service—click here for inquiry and access.

About the Futurum Ecosystems, Channels & Marketplaces Practice

The Futurum Ecosystems, Channels & Marketplaces Practice provides actionable, objective insights for market leaders and their teams so they can respond to emerging opportunities and innovate. Public access to our coverage can be seen here. Follow news and updates from the Futurum Practice on LinkedIn and X. Visit the Futurum Newsroom for more information and insights.

Other Insights from Futurum

A Shift from Technology to Intelligence: The Rise of the Frontier Partner

As Vendors Push More into Their AI Story, Can the Channel Keep Pace?

Cloud Marketplaces – Futurum Signal

Author Information

Tiffani Bova is Chief Strategy and Research Officer at The Futurum Group.

Ranked for the last six years in the Top 50 Business Thinkers in the world by Thinkers50, Tiffani Bova is a thought leader who Forbes says “reshapes our perception of growth.”

As both a practitioner and academic she offers a unique perspective and has helped lead the tech industry through several evolutions over her nearly 30-year career as Salesforce’s former Growth and Innovation Evangelist, and previously as a Distinguished Analyst and Research Fellow at Gartner and a sales, marketing and customer service executive for start-ups and Fortune 500 companies. She is the author of two Wall Street Journal bestsellers: GrowthIQ and The Experience Mindset.

Alex is Vice President & Practice Lead, Ecosystems, Channels, & Marketplaces at the Futurum Group. He is responsible for establishing and maintaining the Channels Research program as part of the overall Futurum GTM and Channels Practice. This includes overseeing the channel data rollout in the Futurum Intelligence Platform, primary research activities such as research boards and surveys, delivering thought-leading research reports, and advising clients on their indirect go-to-market strategies. Alex also supports the overall operations of the Futurum Research Business Unit, including P&L segmentation, sales and marketing alignment, and budget planning.

Prior to joining Futurum, Alex was VP of Channels & Enterprise Research at Canalys where he led a multi-million dollar research organization with more than 20 analysts. He played an integral role in helping the Canalys research organization migrate into Omdia after having been acquired in 2023. He is an accomplished research leader, as well as an expert in indirect go-to-market strategies. He has delivered numerous keynotes at partner-facing conferences.

Alex is based in Portland, Oregon, but has lived in numerous places, including California, Canada, Saudi Arabia, Thailand, and the UK. He has a Bachelor in Commerce and Finance Major from Dalhousie University, Halifax Canada.