Austin, Texas, USA, June 1, 2026

Futurum releases its 1H 2026 Cybersecurity Market Sizing & Five-Year Forecast and Decision Maker Survey of 929 enterprise buyers, sizing the market at $335.8B in 2025 and forecasting $521.7B by 2031, with buyer budget growth moderating rather than reversing.

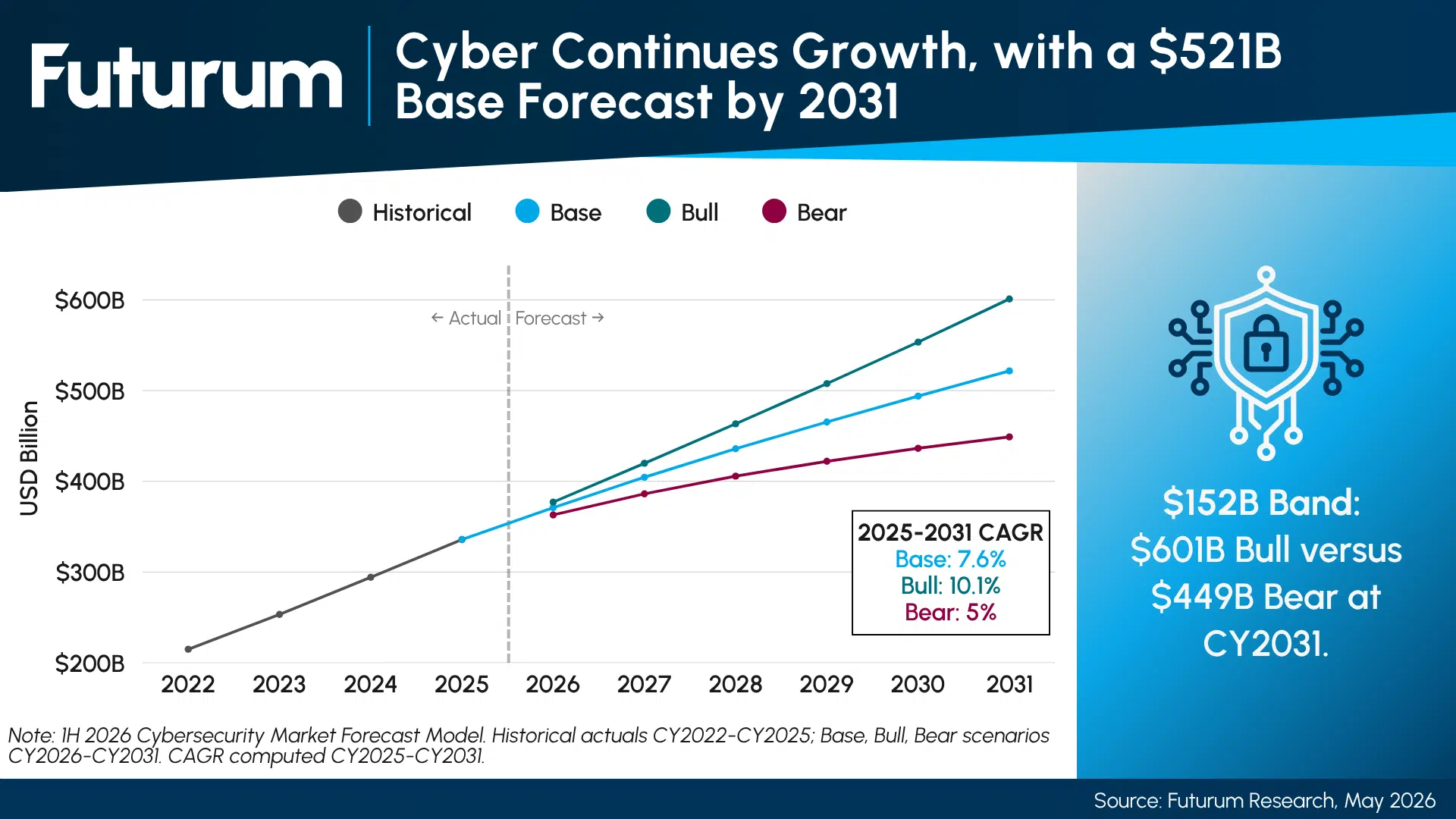

The global cybersecurity market reached $335.8 billion in 2025 and is on track to reach $521.7 billion by 2031 at a 7.6% compound annual growth rate, materially below the 14% to 18% historical trend, according to two new reports released today by The Futurum Group: the “1H 2026 Cybersecurity Market Sizing & Five-Year Forecast” and the “1H 2026 Cybersecurity Decision Maker Survey Report” of 929 global enterprise buyers.

Figure 1: Cybersecurity Market, Historical 2022-2025 and Scenarios 2026-2031

The forecast describes a market decelerating into a contested band. The base case reaches $521.7B by 2031 at 7.6% CAGR; the bull case ($601B, 10.1% CAGR) requires AI security spend to ramp ahead of schedule, accelerated regulatory enforcement, and softer platform-consolidation drag; the bear case ($449B, 5.0% CAGR) is the inverse. All three scenarios describe a market that continues growing in absolute dollars.

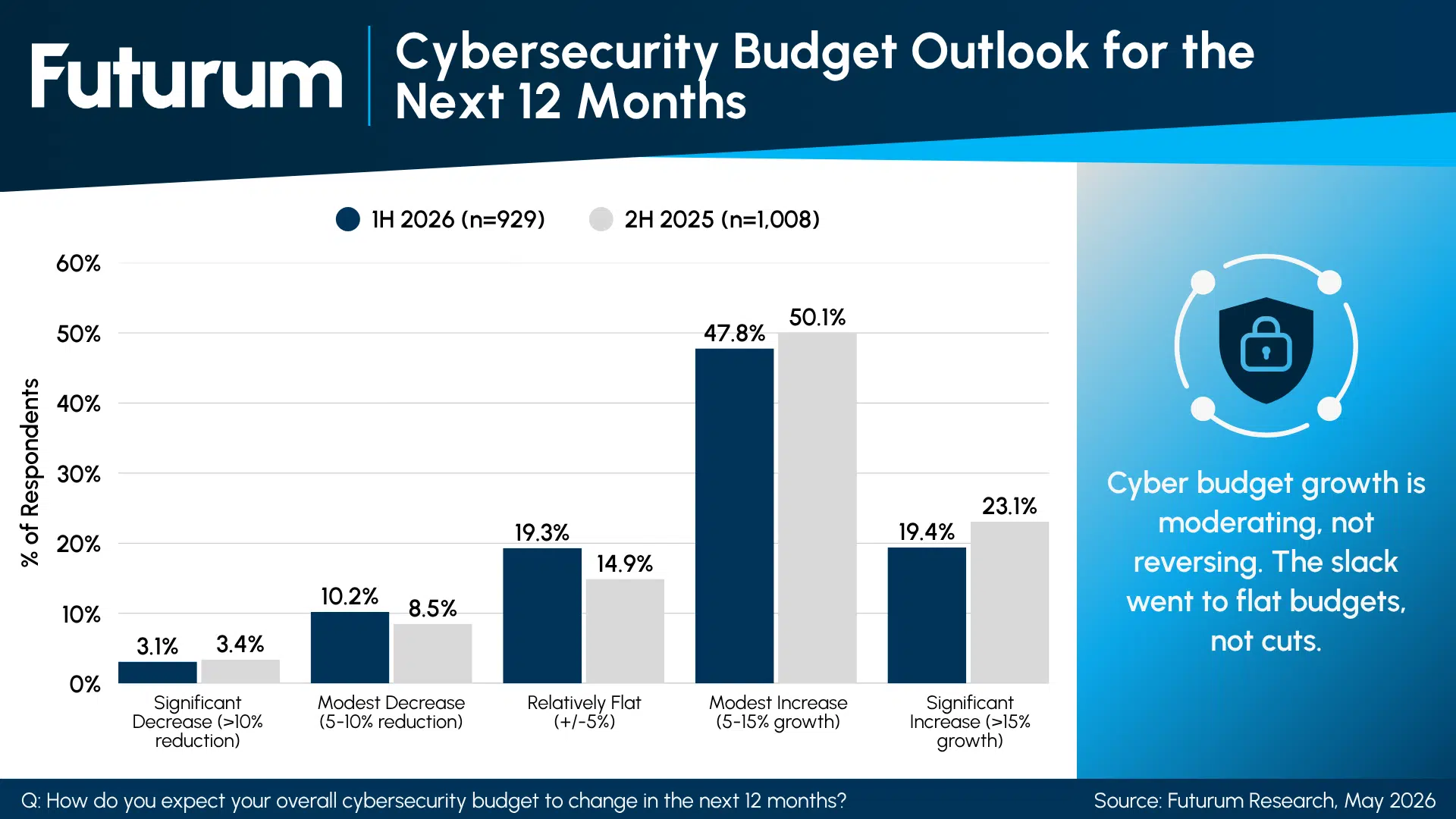

The buyer-side data corroborates the deceleration. 67.2% of organizations anticipate cybersecurity budget increases over the next twelve months (see Figure 2), down six points from 73.2% in 2H 2025. Within increases, the deceleration is concentrated in significant growth (greater than 15%), which fell to 19.4% from 23.1%, while the freed-up share moved into relatively flat budgets (19.3%, up from 14.9%). The decrease tail expanded only modestly.

Figure 2: Cybersecurity Budget Outlook for the Next 12 Months

Fernando Montenegro, VP and Practice Lead for Cybersecurity and Resilience at The Futurum Group, said, “This is a market finishing one expansion cycle and beginning another. The market math and the buyer behavior tell the same story. The story is not about cuts; it is about commitments. Prior-period investments are now in motion, and the dollars that are still moving are being justified on different grounds: enterprise risk discipline rather than infrastructure refresh.”

The reports identify several converging shifts shaping the 1H 2026 cycle:

The four highest-growth segments through 2031 (Cloud Security at 11.8% CAGR, Security Operations & GRC at 10.2%, Data Security at 9.2%, and Application Security at 7.8%) are all directly tied to securing AI workloads and the data feeding them, collectively adding $77 billion of incremental annual spend by 2031.

Buyer threat-concern profiles have pivoted accordingly. Phishing, business email compromise, and AI-driven impersonation (including deepfakes) registered as the second-most-concerning incident type at 25.9% top three, and compromise of non-human identities and service accounts emerged as a notable new category at 13.5%; neither existed in this form in 2H 2025.

Areas such as Identity & Access Management and Endpoint Security registered on the slower side of growth, consistent with a dynamic of seeing platform consolidation pressures as buyers absorb point-tool IAM and endpoint contracts into hyperscaler, SASE, and SecOps platforms. Surveyed organizations with 50,000+ employees report net spend intent roughly 10 points below the benchmark.

Combined vendor consolidation intent rose to 42.0% in 1H 2026 from 34.6% in 2H 2025, while combined expansion intent fell to 35.8% from 43.0%, the first period in this series where consolidation has clearly outpaced expansion.

Among organizations expecting budget growth, risk management strategy now leads the top-cited drivers at 47.8% top three, while cybersecurity modernization fell from 56.0% in 2H 2025 to 44.7% in 1H 2026, an eleven-point decline in mindshare.

The shifts arrive against a more mature governance backdrop. 32.5% of organizations report the CISO into the CIO or CTO, and another 13.8% into the Head of IT, while only 25.5% place the CISO directly under the CEO. At the same time, 65% of organizations now present cybersecurity to the board at least quarterly. Cybersecurity is increasingly board-visible, but structural independence from IT remains uncommon.

“For vendors, the implication is clear,” Montenegro continued. “Reposition go-to-market around AI-security adjacency, not perimeter heritage. Build platform-bundled commercial motions for the largest enterprises while opening a credible mid-market wedge, where Medium Enterprise buyers are growing roughly three times faster than Very Large Enterprise. And anchor vertical pitches to specific regulatory drivers, not generic regulation tailwind. Generic ‘AI-powered’ claims will not move this market; demonstrable, certified integrations and credible AI-defense narratives will.”

Taken together, 1H 2026 describes a cybersecurity function maturing into a more disciplined enterprise practice. Spending is settling into a steadier band, vendor strategies are tightening toward consolidation, governance reporting is becoming routine, and the conversation about threats is being rewritten around AI-shaped attack surfaces.

Read more in the reports “1H 2026 Cybersecurity Market Sizing & Five-Year Forecast” and “1H 2026 Cybersecurity Decision Maker Survey Report” on the Futurum Intelligence Platform.

About Futurum Intelligence for Market Leaders

Futurum Intelligence’s Cybersecurity and Resilience IQ service provides actionable insight from analysts, reports, and interactive visualization datasets, helping leaders drive their organizations through transformation and business growth. Subscribers can log into the Futurum Intelligence platform here, and non-subscribers can find additional information at Futurum Intelligence.

Follow news and updates from Futurum on X and LinkedIn using #Futurum. Visit the Futurum Newsroom for more information and insights.

Other Insights From Futurum:

RSAC 2026: The AI ‘Tragedy of the Commons’ and the Future of Agentic Security

Sovereign AI: What Nations Want (And What They’ll Actually Get)

Are We in a New Westphalian World Web? – Report Summary

Author Information

Fernando Montenegro serves as the Vice President & Practice Lead for Cybersecurity & Resilience at The Futurum Group. In this role, he leads the development and execution of the Cybersecurity research agenda, working closely with the team to drive the practice's growth. His research focuses on addressing critical topics in modern cybersecurity. These include the multifaceted role of AI in cybersecurity, strategies for managing an ever-expanding attack surface, and the evolution of cybersecurity architectures toward more platform-oriented solutions.

Before joining The Futurum Group, Fernando held senior industry analyst roles at Omdia, S&P Global, and 451 Research. His career also includes diverse roles in customer support, security, IT operations, professional services, and sales engineering. He has worked with pioneering Internet Service Providers, established security vendors, and startups across North and South America.

Fernando holds a Bachelor’s degree in Computer Science from Universidade Federal do Rio Grande do Sul in Brazil and various industry certifications. Although he is originally from Brazil, he has been based in Toronto, Canada, for many years.