Austin, Texas, USA, May 18, 2026

The Futurum Group today released the “1H 2026 Data Center Semiconductor Decision Maker Survey Report,” a global study of 824 procurement decision makers and strong influencers shaping enterprise data center semiconductor buying in 2026. The findings show a market in transition, with reasoning model workloads becoming the primary target of compute allocation and a new set of token economics benchmarks reshaping how data center semiconductor vendors are evaluated.

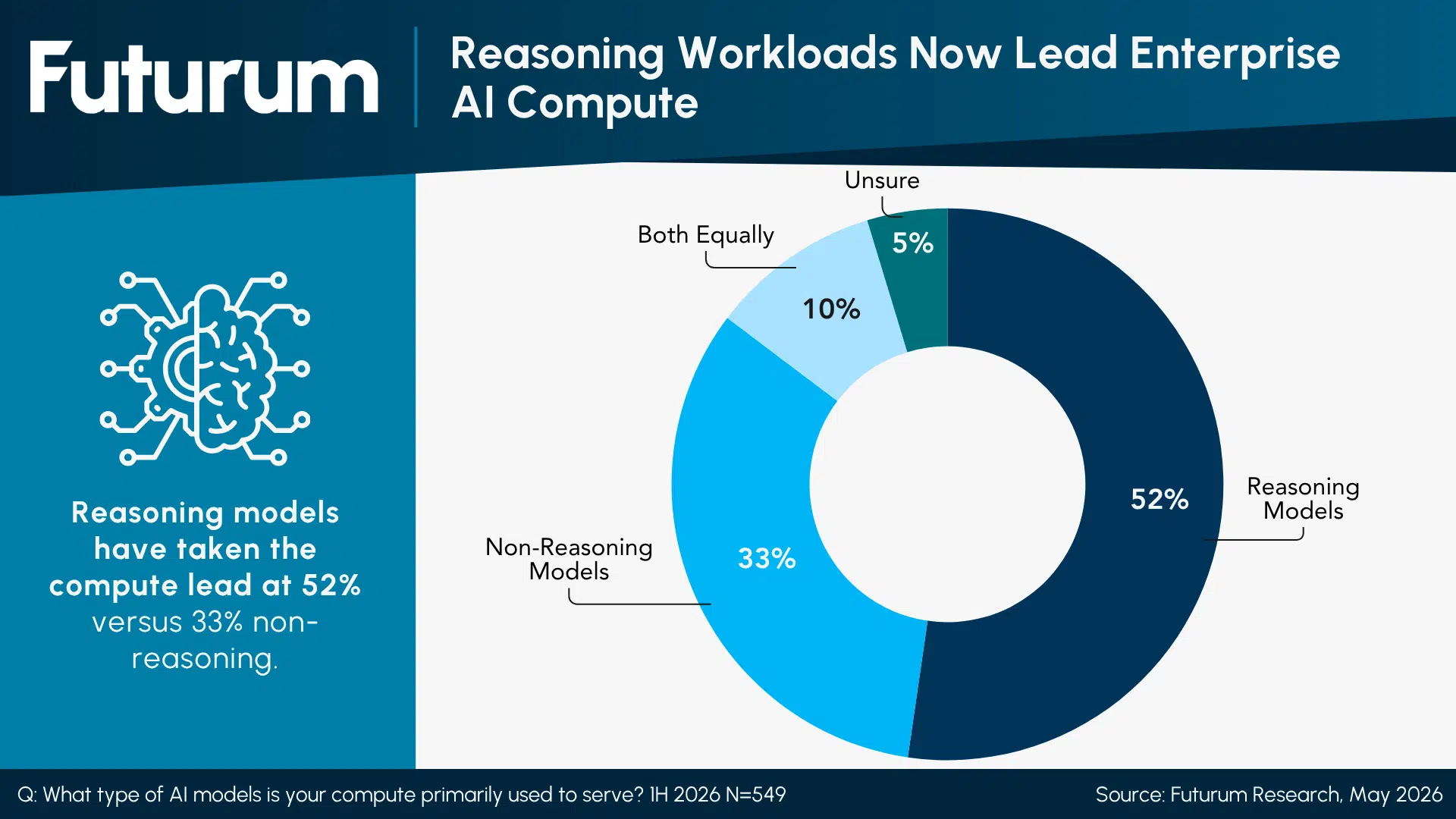

The defining finding of the 1H 2026 survey is the composition of AI workloads. Among the 549 decision makers serving model traffic, 52.3% report that their compute is primarily devoted to reasoning models, compared with 33.0% on non-reasoning models. Across the full sample, 54.0% describe their AI workload as balanced between training and inference, with only 20.5% identifying as mostly-inference workloads. Buyers reinforce that they are still training and fine-tuning models in roughly equal measure to running them at scale.

Figure 1: Reasoning Workloads Now Lead Enterprise AI Compute

“Changing AI model types encourages compute buyers to rethink semiconductor investment decisions,” said Brendan Burke, Research Director for Semiconductors, Supply Chain, and Emerging Tech at The Futurum Group. “Reasoning models are now the primary model type served by a majority of compute decision makers, encouraging cost and latency reduction. These changing parameters align with outsized expectations for usage of GPU alternatives, including CPUs and XPUs. Vendors in the data center semiconductor stack need to influence efficiency metrics, including tokens per watt and time to first production token to serve buyer priorities.”

The shift in workload composition is forcing a parallel shift in how data center semiconductor infrastructure is measured. 35.2% of decision makers now use tokens per watt as their primary productivity benchmark, ahead of time-to-train (25.8%), $/FLOP (25.1%), and hardware utilization (13.8%). 60.3% target 500,000 or more tokens per second per megawatt, and 54.7% already generate 51 trillion or more tokens annually. Token-denominated metrics have moved from analyst framing into operational targets, and the data center semiconductor companies that can credibly anchor their roadmap to these benchmarks have a defensible position in the next 24 months.

On the supply side, the constraint picture has flipped year over year. Budget and CapEx limits are now the top scaling barrier at 23.3%, up from 14.9% in 2H 2025, while chip supply has fallen from 25.6% to 12.4%. Power and cooling availability (14.9%), networking lead times (16.6%), and grid interconnection capacity (16.6% of cluster expansion limits) collectively rival silicon as binding constraints on growth. For data center semiconductor planning, capital and physical infrastructure have replaced raw chip availability as the dominant question.

Key Findings

- Reasoning Models Lead Model-Serving Compute: 52.3% of decision makers serving model traffic report that their compute is primarily devoted to reasoning models, versus 33.0% on non-reasoning models, with 10.0% serving both equally.

- Workload Mix Remains Balanced Between Training and Inference: 54.0% of decision makers describe their AI workload as balanced between training and inference, only 20.5% report mostly-inference workloads, and 25.5% remain training-dominant, indicating that the inference inflection remains in a transitional phase.

- Tokens per Watt Is the New Productivity Benchmark: 35.2% of decision makers now use tokens per watt as their primary AI infrastructure productivity metric, ahead of time-to-train (25.8%), $/TFLOP (25.1%), and hardware utilization (13.8%). 60.3% target 500,000 or more tokens per second per megawatt.

- Capital Has Replaced Chip Supply as the Top Scaling Constraint: Budget and CapEx limits rose to 23.3% of decision makers in 1H 2026 from 14.9% in 2H 2025, while chip supply fell from 25.6% to 12.4%. The binding constraint on data center semiconductor scale-out has shifted from silicon availability to capital and physical infrastructure.

The full “1H 2026 Data Center Semiconductor Decision Maker Survey Report” is available now for Futurum Intelligence subscribers. Non-subscribers can click here for more information and subscription details.

About Futurum Intelligence for Market Leaders

Futurum Intelligence’s Data Center Semiconductors service provides actionable insight from analysts, reports, and interactive visualization datasets, helping leaders drive their organizations through transformation and turn disruption into a competitive advantage. The Futurum Group’s analysts, researchers, and advisors help business leaders anticipate tectonic shifts in their industries and leverage disruptive innovation.

Follow news and updates from Futurum on X and LinkedIn using #Futurum. Visit the Futurum Newsroom for more information and insights.

Other Insights from Futurum:

Coherent Q3 FY 2026: AI Data Center Demand Accelerates Optical Growth

Astera Labs Q1 FY 2026 Earnings Highlight Scale-Up Switching Ramp

Can OpenAI’s MRC Networking Protocol Redefine the Economics of AI Training?

Author Information

Brendan is Research Director, Semiconductors, Supply Chain, and Emerging Tech. He advises clients on strategic initiatives and leads the Futurum Semiconductors Practice. He is an experienced tech industry analyst who has guided tech leaders in identifying market opportunities spanning edge processors, generative AI applications, and hyperscale data centers.

Before joining Futurum, Brendan consulted with global AI leaders and served as a Senior Analyst in Emerging Technology Research at PitchBook. At PitchBook, he developed market intelligence tools for AI, highlighted by one of the industry’s most comprehensive AI semiconductor market landscapes encompassing both public and private companies. He has advised Fortune 100 tech giants, growth-stage innovators, global investors, and leading market research firms. Before PitchBook, he led research teams in tech investment banking and market research.

Brendan is based in Seattle, Washington. He has a Bachelor of Arts Degree from Amherst College.