Analyst(s): Brendan Burke

Publication Date: March 23, 2026

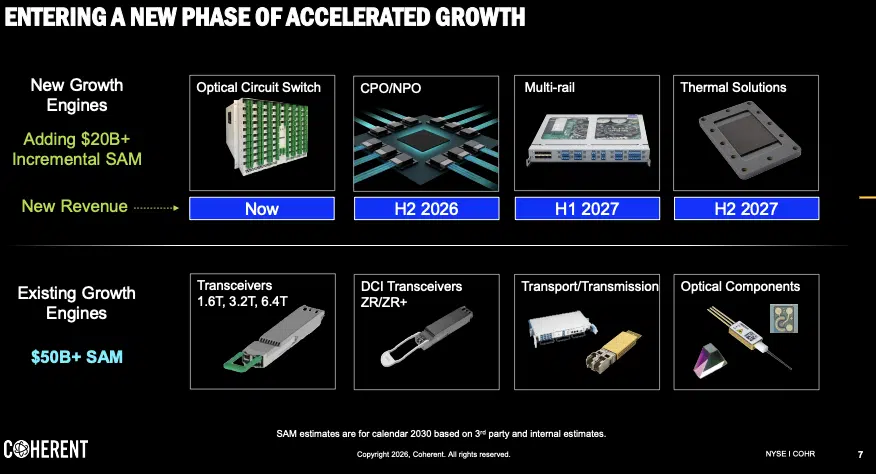

Coherent Corp. used its OFC 2026 investor presentation to raise its co-packaged optics (CPO) serviceable addressable market (SAM) to $15 billion, double its optical circuit switch (OCS) SAM to $4 billion, and introduce a $2 billion thermal management SAM, bringing its combined growth segment opportunity to over $23 billion. The SAM expansion aligns directly with NVIDIA’s public commitment to integrating 200 Gb/s CPO silicon photonics into its Spectrum-6 switching platform and scaling direct optical interconnects through Kyber into the NVL1152 supercomputer architecture.

What is Covered in This Article:

- Coherent’s $21 billion combined data center SAM framework at OFC 2026

- NVIDIA’s Spectrum-6 and Kyber as structural demand catalysts for CPO

- The doubling of the OCS SAM from $2 billion to $4 billion on broadened use cases

- Indium phosphide capacity expansion and the 6-inch wafer transition at scale

- Thermal materials are an emerging data center revenue line tied to power constraints

The News: Coherent presented its updated data center product roadmap at the Optical Fiber Communication Conference (OFC) in March 2026, disclosing a series of SAM revisions that collectively frame a $21 billion addressable opportunity across three product categories. The company raised its CPO SAM to $15 billion, encompassing external laser source (ELS) modules, high-power continuous wave (CW) lasers, photonic integrated circuits (PICs), fiber attach units, isolators, thermoelectric coolers, and polarization-maintaining lens arrays (PMLAs). It doubled its OCS SAM from $2 billion to $4 billion, citing broader use cases across scale-up, scale-out, scale-across, and spine applications, along with faster-than-expected customer adoption across more than 10 shipping customers. Separately, Coherent placed a $2 billion SAM on its thermal management materials business for the first time, anchored by Thermadite—a proprietary diamond silicon carbide ceramic—and a separate $2 billion SAM on multi-rail transport equipment.

The SAM disclosures arrived alongside operational updates on indium phosphide manufacturing, where the company confirmed plans to double capacity in calendar year 2026 and double again thereafter, with nearly all incremental capacity on 6-inch wafer lines. CEO Jim Anderson disclosed that a $2 billion investment from NVIDIA would fund a substantial portion of this expansion, with the supply agreement covering multiple CPO-related products through the rest of the decade. Anderson stated that CPO revenue for scale-out applications would begin in the second half of calendar 2026, followed by scale-up CPO revenue starting in the second half of 2027.

Coherent’s $23 Billion Growth Opportunity Lifted by NVIDIA’s Optical Ambitions

Analyst Take: Coherent Corp. (COHR) presented its updated data center product roadmap at the Optical Fiber Communication Conference (OFC) in March 2026, disclosing a series of SAM revisions that collectively frame a $21 billion addressable opportunity across three product categories. The company raised its CPO SAM to $15 billion, encompassing external laser source (ELS) modules, high-power continuous wave (CW) lasers, photonic integrated circuits (PICs), fiber attach units, isolators, thermoelectric coolers, and polarization-maintaining lens arrays (PMLAs).

The company doubled its OCS SAM from $2 billion to $4 billion, citing broader use cases across scale-up, scale-out, scale-across, and spine applications, along with faster-than-expected customer adoption across more than 10 shipping customers. Separately, Coherent placed a $2 billion SAM on its thermal management materials business for the first time, anchored by Thermadite, a proprietary diamond silicon carbide ceramic, and silicon carbide substrates targeting heat dissipation and energy reclamation in AI data centers.

The SAM disclosures arrived alongside operational updates on indium phosphide manufacturing, where the company confirmed plans to double capacity in calendar year 2026 and double again thereafter, with nearly all incremental capacity on 6-inch wafer lines. CEO Jim Anderson disclosed that a $2 billion investment from NVIDIA would fund a substantial portion of this expansion, with the supply agreement covering multiple CPO-related products through the rest of the decade. Anderson stated that CPO revenue for scale-out applications would begin in the second half of calendar 2026, followed by scale-up CPO revenue starting in the second half of 2027.

Coherent’s OFC disclosure is significant not because the company raised its TAM projections but because the timing and structure of these revisions map directly onto a visible, vendor-confirmed architectural transition at NVIDIA. NVIDIA’s Spectrum-6 switch’s integration of 200 Gb/s co-packaged optics in single- and multi-chip configurations replaces pluggable transceivers entirely, creating a structural procurement requirement for the exact portfolio of components Coherent presented: indium phosphide CW lasers, ELS modules, fiber attach assemblies, and semiconductor optical amplifiers. That NVIDIA has committed $2 billion in capital to Coherent and signed a multi-product supply agreement through the rest of the decade converts what might otherwise be a speculative TAM exercise into something closer to a forward order book, at least for the NVIDIA share of the opportunity.

CPO SAM in Context: The $15 Billion Question

The $15 billion CPO SAM deserves scrutiny not for its size but for how Coherent arrives at it. Unlike transceiver vendors whose addressable market is defined by module volumes and pricing, Coherent’s CPO opportunity is a bill-of-materials play. The company positions itself as a supplier of components for the CPO module rather than the module itself, spanning lasers, amplifiers, isolators, coolers, fiber attach units, and PMLAs. Anderson emphasized that no other supplier in the world brings that entire portfolio of technology, and that customers working with Coherent obtain a one-stop-shop supply chain rather than having to integrate across multiple vendors.

This breadth argument has commercial merit. CPO integration is substantially more complex than pluggable transceiver assembly, and hyperscalers designing systems around NVIDIA’s Spectrum-6 or Broadcom’s Tomahawk 6 face supply chain coordination challenges that favor consolidated suppliers. However, the $15 billion figure remains a SAM rather than a revenue forecast, and Coherent has not broken it down to component-level granularity, noting only that the ELS module and fiber attach unit represent the two largest portions. The gap between a $15 billion addressable market and actual revenue capture will depend on competitive dynamics, yield ramp performance on 6-inch indium phosphide, and the pace at which CPO displaces pluggable optics across the data center.

NVIDIA’s Architectural Tailwind Brings Clarity to the Opportunity

The alignment between Coherent’s roadmap and NVIDIA’s published architecture is more concrete than is typical for vendor-supplier relationships in the optical space. NVIDIA’s Spectrum-6 SPX rack integrates CPO at the switch level, replacing pluggable transceivers to deliver what NVIDIA describes as the highest power efficiency, nearly perfect effective bandwidth, and low latency and jitter for synchronizing AI workloads. The Kyber interconnect fabric, which will first appear with Vera Rubin Ultra as an NVL144 system before scaling to NVL576 and ultimately NVL1152, relies on direct optical interconnects for rack-to-rack scale-up. This creates a multi-year demand trajectory that extends well beyond the initial Spectrum-6 ramp.

We expect industry demand for 1.6T optical modules to grow from 1.8 million units in 2025 to over 30 million units in 2026, with NVIDIA accounting for over 60% of that demand, and Google and Meta comprising the remainder. Coherent’s indium phosphide capacity expansion—doubling in 2026 and 2027, nearly all on 6-inch lines—is calibrated to this ramp. Each 6-inch wafer yields more than 4 times as many devices as a 3-inch wafer, and by the end of 2026, Coherent expects a 50-50 mix of 3-inch and 6-inch capacity, with 6-inch dominating incremental additions thereafter.

Optical Circuit Switches: From Niche to Network Fabric

The doubling of the OCS SAM from $2 billion to $4 billion reflects a broader reframing of optical circuit switching. Chief Technology Officer Julie Eng described OCS not as a replacement for electrical packet switching, but as a new capability in the data center—one that allows operators to send a software command and reconfigure how all fibers are connected within anything touching the OCS. The initial use case was spine switch replacement, publicly associated with Google. But Eng stated that use cases have expanded to scale-up, scale-out, scale-across, and spine, driven by the realization that software-defined fiber reconfiguration allows operators to optimize GPU utilization on a per-job basis.

The economic rationale is that XPU costs are high, and the ability to reconfigure network topology at software speeds to maximize GPU utilization has direct revenue implications for data center operators. Coherent’s liquid crystal-based OCS technology, which operates at under 10 volts compared to 100-200 volts for competing MEMS-based approaches, offers differentiated reliability characteristics that customers have publicly acknowledged. The company is shipping 64×64 and 320×320 systems into production and is developing a 512×512 system.

Thermal Materials: A New Revenue Vector With High Barriers

The $2 billion thermal management SAM represents the most nascent of Coherent’s three opportunity areas, but it may also be the most defensible. Thermadite, a proprietary diamond silicon carbide ceramic, transfers heat at twice the efficiency of copper cold plates. Eng stated that simulation and measurement data show the material can reduce XPU junction temperatures by 5 to 10 degrees Celsius, which customers are expected to use not for reliability margin but to run at higher clock speeds and increase compute output. A second application uses thermoelectric coolers in reverse to convert waste heat into electricity that is fed back into the data center. Revenue is expected to begin in the second half of calendar 2027.

Anderson characterized the barriers to entry as very high, comparing the challenge of reverse-engineering Thermadite’s material composition to reproducing a recipe without instructions. Combined with the $15 billion CPO SAM, the $4 billion OCS SAM, and $2 billion for multi-rail, the thermal materials opportunity brings Coherent’s total declared growth opportunity to $21 billion, a figure that frames the company’s ambition to evolve from a component supplier into a full-stack photonics and materials platform for AI infrastructure.

What to Watch:

- Broadcom Tomahawk 6 CPO competition. Broadcom’s third-generation CPO technology, announced in October 2025, targets the same 200 Gb/s silicon photonics integration as NVIDIA’s Spectrum-6. Whether Broadcom sources CPO components from Coherent or builds a vertically integrated alternative will determine how much of the $15 billion CPO SAM Coherent can access beyond the NVIDIA supply agreement.

- LPO as a delay mechanism for CPO adoption. Linear pluggable optics (LPO), championed by Arista Networks, preserve existing switch form factors and may defer CPO transitions, slowing Coherent’s ramp timeline.

- Indium phosphide 6-inch wafer yield at scale. Coherent’s plan to double capacity in 2026 and again thereafter depends on achieving production-grade yields on 6-inch indium phosphide wafers, a transition the broader industry has not yet completed at volume. Any yield shortfall would directly constrain Coherent’s ability to fulfill the NVIDIA supply agreement and could open the share for competing laser suppliers such as Lumentum or nLIGHT.

- 1.6T optical module demand as a CPO transition indicator. The pace of that migration will determine whether Coherent’s new CPO revenue is additive to its existing transceiver business or begins to cannibalize it.

- Thermal management validation against liquid cooling alternatives. Coherent’s Thermadite thermal interface must compete with established suppliers such as Henkel and Shin-Etsu, as well as with the rapid expansion of direct liquid-cooling solutions.

See the complete presentation from Coherent Corp. at OFC 2026 on the Coherent investor relations website.

Disclosure: Futurum is a research and advisory firm that engages or has engaged in research, analysis, and advisory services with many technology companies, including those mentioned in this article. The author does not hold any equity positions with any company mentioned in this article.

Analysis and opinions expressed herein are specific to the analyst individually and data and other information that might have been provided for validation, not those of Futurum as a whole.

Other Insights from Futurum:

Coherent Q2 FY 2026: AI Datacenter Demand Lifts Revenue and Margins

Did SPIE Photonics West 2026 Set the Stage for Scale-up Optics?

Coherent Q1 FY 2026 Shows Strong Datacenter & Comms Momentum

Author Information

Brendan is Research Director, Semiconductors, Supply Chain, and Emerging Tech. He advises clients on strategic initiatives and leads the Futurum Semiconductors Practice. He is an experienced tech industry analyst who has guided tech leaders in identifying market opportunities spanning edge processors, generative AI applications, and hyperscale data centers.

Before joining Futurum, Brendan consulted with global AI leaders and served as a Senior Analyst in Emerging Technology Research at PitchBook. At PitchBook, he developed market intelligence tools for AI, highlighted by one of the industry’s most comprehensive AI semiconductor market landscapes encompassing both public and private companies. He has advised Fortune 100 tech giants, growth-stage innovators, global investors, and leading market research firms. Before PitchBook, he led research teams in tech investment banking and market research.

Brendan is based in Seattle, Washington. He has a Bachelor of Arts Degree from Amherst College.