Austin, Texas, USA, March 4, 2026

The Futurum Group today released findings from its “1H 2026 Ecosystems, Channels & Marketplaces Global Enterprise Decision Maker Survey Report,” a study of 400 technology channel partner decision-makers that reveals a decisive shift in how partners engage with vendors: channel partner co-sell support has surged to the number one vendor priority, while traditional enablement programs have collapsed to the bottom of the list.

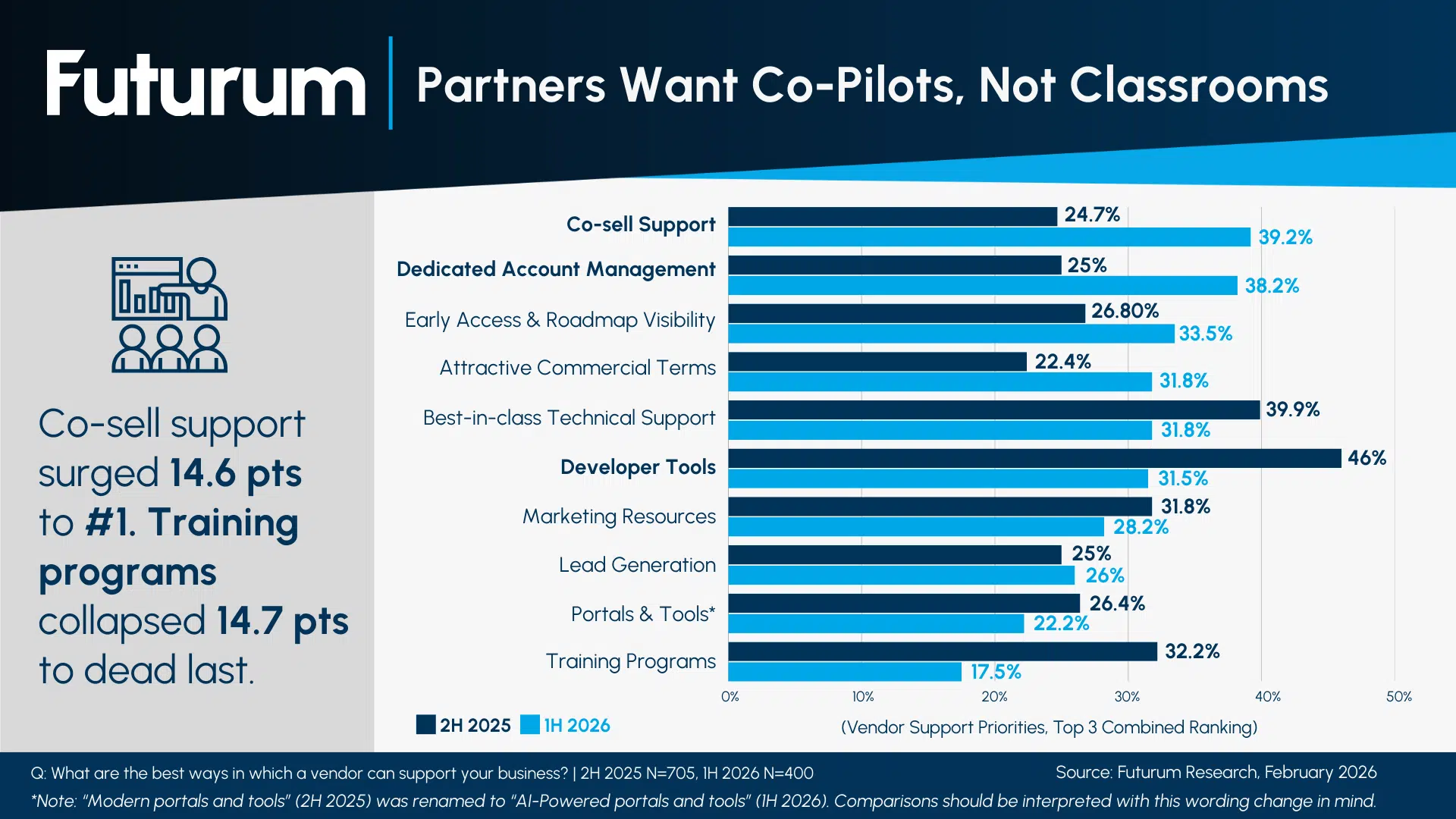

The study, benchmarked against a 2H 2025 baseline of 705 respondents, found that co-sell support jumped 14.6 percentage points to 39.2%, displacing developer tools as the top vendor support priority. Dedicated account management rose 13.3 points to 38.2%. In the sharpest decline, training programs fell 14.7 percentage points to just 17.5%, dropping to dead last among all ten support categories. Developer tools, previously the number one priority, fell 14.5 points to 31.5%. Partners are no longer asking vendors to teach them — they are asking vendors to sell with them.

The demand for channel partner co-sell engagement coincides with a dramatic rise in internal anxiety. “Lack of portfolio competitiveness” more than doubled as a top-three business challenge, surging 17.7 percentage points to 32.5% — the largest swing of any data point in the study. Meanwhile, macroeconomic concerns receded sharply: “challenging economy” dropped 11.7 points, “complex regulatory environment” fell 10.5 points, and “supply chain challenges” declined 9.8 points. Partners have shifted from worrying about external headwinds to questioning whether their own offerings can compete in an AI-reshaped market.

Figure 1: Partners Want Co-Pilots, Not Classrooms — Vendor Support Priorities, Top 3 Combined Ranking

AI maturity is also evolving. Overall AI confidence held steady at 83%, but beneath that stable headline, operational indicators are rising while aspirational ones are falling. Partners developing their own AI solutions using LLMs climbed 4.2 points to 50.8%, and those reporting a “robust AI business generating significant revenue” rose 4.5 points to 48.0%. Meanwhile, “strong brand reputation in AI” dropped 4.6 points, and “AI central to strategy” fell 3.2. AI is transitioning from a strategic positioning play to an operational revenue driver.

The vendor landscape is reshuffling accordingly. Oracle (+8.3 pts), Dell (+7.7), and Lenovo (+7.1) posted the largest strategic gains, driven by AI-related infrastructure demand. IBM (−6.6 pts), Adobe (−6.2), and VMware by Broadcom (−4.4) saw the steepest declines. Microsoft (67.2%), AWS (62.5%), and Google Cloud (52.0%) remain the dominant anchors.

Despite moderated growth expectations — strong growth above 10% dropped from 59.4% to 36.0% — partners are investing counter-cyclically. Net hiring intentions held at 72.2%, and acquisition activity rose to 20.2%. The channel is not contracting; it is repositioning for an AI-defined future.

“Overall, partners remain optimistic about 2026,” said Alex Smith, Vice President & Practice Lead, Ecosystems, Channels, and Marketplaces at The Futurum Group. “However, under the hood, the needs of partners are changing. The importance of co-sell in conjunction with the fears about their portfolio competitiveness shows that partners want to be tightly aligned with vendors as they look to capitalize in an era of AI.”

- Co-Sell Surge: Co-sell support jumped 14.6 percentage points to become the number one vendor support priority at 39.2%, while training programs collapsed 14.7 points to dead last at 17.5%.

- Portfolio Panic: “Lack of portfolio competitiveness” more than doubled as a top-three business challenge (+17.7 pts to 32.5%), the largest swing of any ranked data point in the study.

- AI Revenue Maturation: Among confident partners, 48.0% now report a robust AI business generating significant revenue (+4.5 pts), and 50.8% have developed their own AI solutions using LLMs (+4.2 pts).

- Infrastructure Vendors Gaining Ground: Oracle (+8.3 pts), Dell (+7.7), and Lenovo (+7.1) posted the largest strategic vendor gains, driven by AI-related hardware and data center demand.

- Counter-Cyclical Investment: Despite strong growth expectations dropping from 59.4% to 36.0%, net hiring held at 72.2% and acquisition activity rose to 20.2%, signaling partners are positioning for 2027 and beyond.

The full “1H 2026 Ecosystems, Channels & Marketplaces Global Enterprise Decision Maker Survey Report” is available now for Futurum Intelligence subscribers. Non-subscribers can click here for more information.

About Futurum Intelligence for Market Leaders

Futurum Intelligence’s IQ service provides actionable insight from analysts, reports, and interactive visualization datasets, helping leaders drive their organizations through transformation and business growth. Subscribers can log into the platform at https://app.futurumgroup.com/, and non-subscribers can find additional information at Futurum Intelligence.

Follow news and updates from Futurum on X and LinkedIn using #Futurum. Visit the Futurum Newsroom for more information and insights.

Other Insights From Futurum:

Can Writer’s Partner Program Model Scale Enterprise AI Through Ecosystem Rigor?

Proofpoint Increases Bets on Partners to Capture More Security Mindshare

Hyperscaler Marketplace Spending Surges as Enterprises Shift Software Budgets

Author Information

Alex is Vice President & Practice Lead, Ecosystems, Channels, & Marketplaces at the Futurum Group. He is responsible for establishing and maintaining the Channels Research program as part of the overall Futurum GTM and Channels Practice. This includes overseeing the channel data rollout in the Futurum Intelligence Platform, primary research activities such as research boards and surveys, delivering thought-leading research reports, and advising clients on their indirect go-to-market strategies. Alex also supports the overall operations of the Futurum Research Business Unit, including P&L segmentation, sales and marketing alignment, and budget planning.

Prior to joining Futurum, Alex was VP of Channels & Enterprise Research at Canalys where he led a multi-million dollar research organization with more than 20 analysts. He played an integral role in helping the Canalys research organization migrate into Omdia after having been acquired in 2023. He is an accomplished research leader, as well as an expert in indirect go-to-market strategies. He has delivered numerous keynotes at partner-facing conferences.

Alex is based in Portland, Oregon, but has lived in numerous places, including California, Canada, Saudi Arabia, Thailand, and the UK. He has a Bachelor in Commerce and Finance Major from Dalhousie University, Halifax Canada.