Analyst(s): Richard Gordon

Publication Date: April 24, 2025

The dismantling of the hyper-globalized semiconductor supply chain is underway, and recent global events will accelerate the trend. What replaces it will fundamentally restructure the industry and how it operates, forcing semiconductor companies to change the way they do business.

Key Points:

- Deglobalization of the hyper-globalized semiconductor supply chain is underway, prompted by single-point-of-failure vulnerabilities exposed by recent global events.

- As the U.S./China technology arms race hots up, increased geopolitical tensions and challenges to the post-war consensus on international trade will accelerate the process.

- Critical gaps in regional capabilities will constrain the emergence of restructured, regionalized semiconductor supply chains.

Overview:

The semiconductor industry has long relied on a highly globalized supply chain, which has enabled cost efficiency, faster innovation, and rapid time-to-market. Key factors driving this globalization included a shared technological roadmap, low-cost manufacturing hubs, specialization through the fabless-foundry model, and post-war political commitment to free trade. However, recent global events—natural disasters, COVID-19, and geopolitical tensions—have exposed the fragility of this system and highlighted the risks of single points of failure.

Single Points of Failure in the Global Semiconductor Supply Chain

The most critical vulnerability lies in advanced chip manufacturing, where Taiwan’s TSMC plays an outsized role. Additionally, China dominates the supply of rare earth materials, while Europe is home to essential lithography equipment providers, such as ASML. The U.S. depends heavily on these regions for key elements of semiconductor production.

U.S.-China Technology Arms Race

A major factor accelerating deglobalization is the U.S.-China technology arms race. Since 2019, the U.S. has imposed strict export controls on China, blacklisted tech firms such as Huawei and SMIC, and restricted China’s access to critical semiconductor tools, particularly EUV lithography. The goal is to limit China’s technological advancement and protect U.S. national security.

Shifting U.S. Geopolitical Stance

The shift in U.S. policy intensified under President Trump’s 2025 administration, which introduced protectionist trade policies and sweeping tariffs. This signals a strategic push toward technological sovereignty and domestic resilience, encouraging the reshoring of semiconductor manufacturing.

Regional Supply Chains

Deglobalization is leading to the emergence of regional supply chains supported by initiatives such as the U.S. CHIPS Act and the EU’s Chips Act.

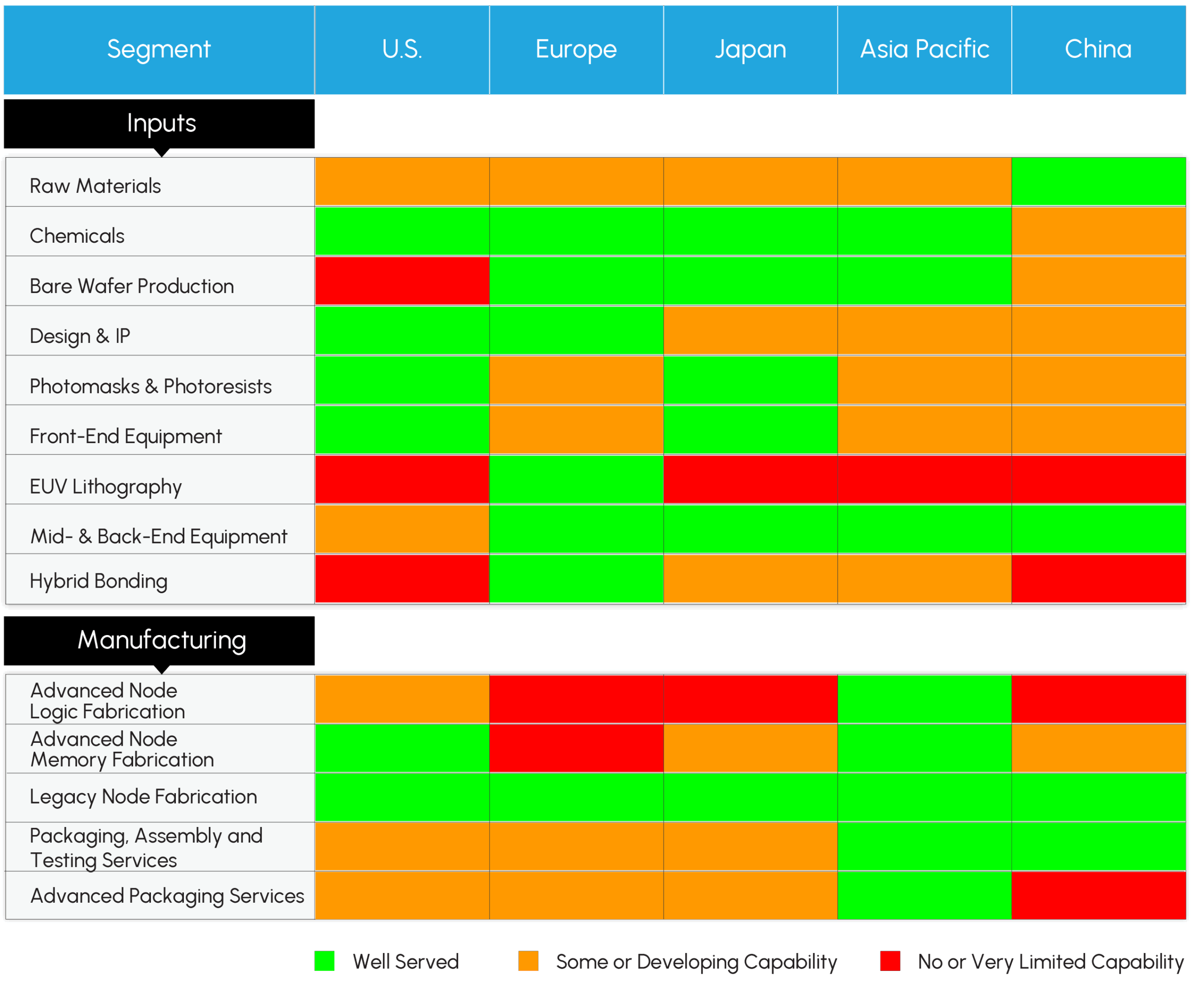

However, regions face significant capability gaps. For example, the U.S. lacks bare wafer production and advanced packaging capacity; Europe lacks leading-edge fabs; Japan lacks EUV lithography; and China faces export restrictions on advanced chipmaking tools.

Table 1. Regional Semiconductor Supply Chain Capability Gaps

The transformation from globalized to regionalized supply chains will likely result in higher production and transportation costs, slower innovation, and increased product prices. Globalization’s efficiency and innovation gains are being traded for resilience, national security, and geopolitical leverage.

To adapt, semiconductor companies are advised to diversify their supply chains regionally, pursue vertical integration, invest in R&D, align with government incentives, and strengthen relationships with critical suppliers. Emerging markets such as India also have a growing opportunity to enter the semiconductor space.

Conclusion

In conclusion, the global semiconductor landscape is undergoing a profound restructuring. Driven by geopolitical rivalry, particularly between the U.S. and China, and a strategic U.S. policy shift, the industry is moving toward regionalized supply chains. While this may reduce geopolitical risk and improve national resilience, it brings substantial trade-offs in cost, efficiency, and innovation speed. Companies must adapt swiftly to remain competitive in this new, fragmented environment.

The full report is available via subscription to the Semiconductors IQ service from Futurum Intelligence—click here for inquiry and access.

Futurum clients can read more about it in the Semiconductors Intelligence Platform, and non-clients can learn more here: Semiconductors Practice.

About the Futurum Semiconductors Practice

The Futurum Semiconductors Practice provides actionable, objective insights for market leaders and their teams so they can respond to emerging opportunities and innovate. Public access to our coverage can be seen here. Follow news and updates from the Futurum Practice on LinkedIn and X. Visit the Futurum Newsroom for more information and insights.

Author Information

Richard is a sought-after technology industry analyst, both as a trusted advisor to clients and also as an expert commentator speaking at industry events and appearing on live TV shows such as CNBC.