Austin, Texas, USA, April 24, 2026

Futurum Research finds that nearly half of organizations identify accelerator supply and power availability as their biggest constraints to scaling data center compute, according to a survey of key decision-makers.

GPU supply shortages and power/cooling limitations have emerged as the dominant barriers preventing organizations from scaling their data center compute infrastructure, according to a comprehensive decision-maker survey from The Futurum Group.

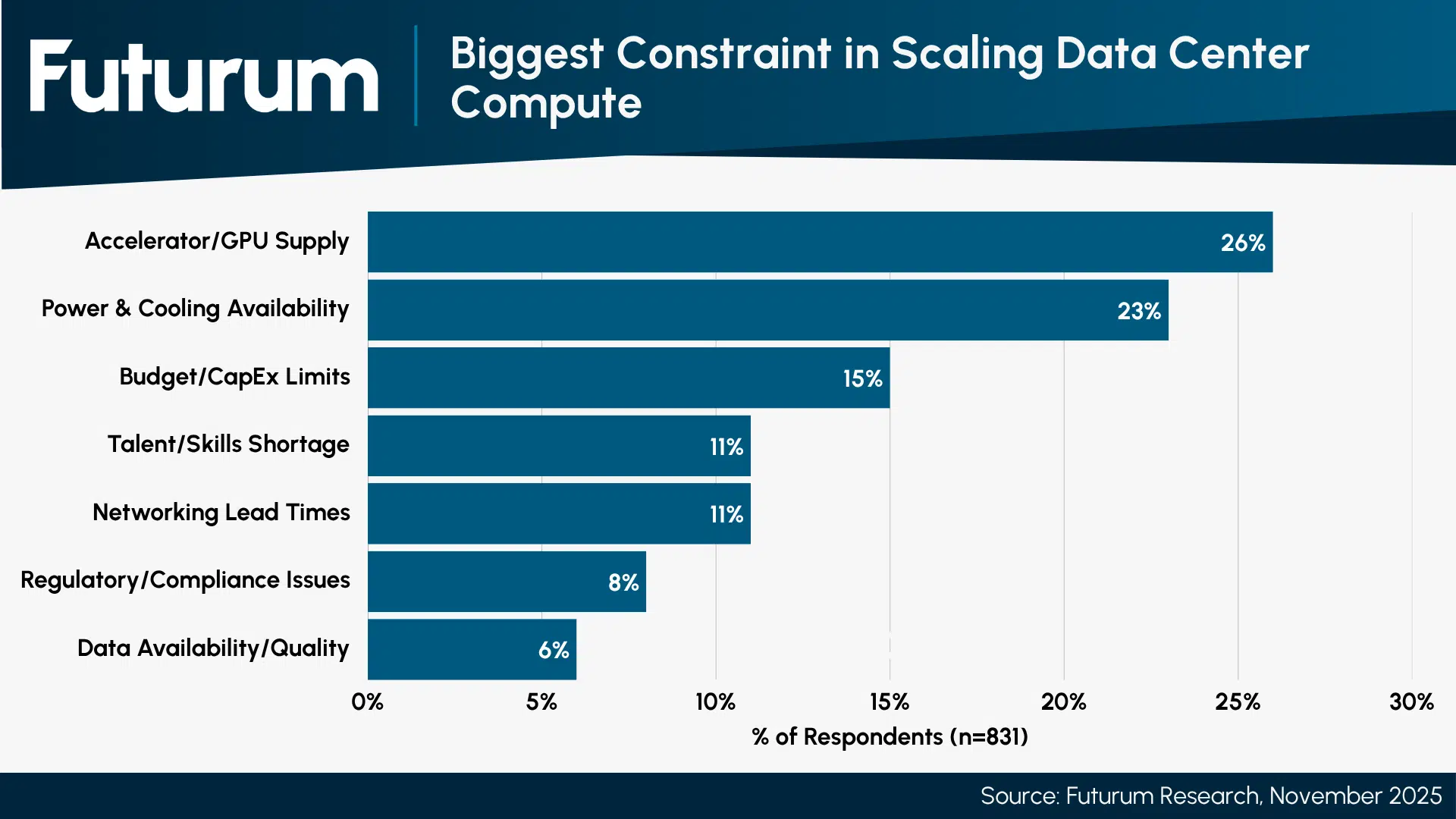

The Futurum Data Center Semiconductors Decision Maker Survey reveals that a combined 49% of organizations cite accelerator/GPU supply (26%) or power & cooling availability (23%) as their single biggest constraint, signaling that AI compute demand continues to vastly outstrip available infrastructure capacity.

Figure 1: Biggest Constraint in Scaling Data Center Compute

Brendan Burke, Research Director, Semiconductors, Supply Chain & Emerging Tech at Futurum, said, “The fact that accelerator supply and power availability together account for nearly half of all scaling constraints tells us that structural realities will define compute investment decisions for years to come.”

The research reveals several key developments shaping the data center semiconductors landscape:

- Chip supply is the single largest bottleneck: 26% of organizations identify accelerator/GPU supply as their top constraint in scaling data center compute, reflecting persistent supply-demand imbalances.

- Power and cooling are a binding ceiling: 23% cite power and cooling availability as their primary constraint — an infrastructure limitation that cannot be resolved with capital alone.

- Budget and talent form a second tier of constraints: Budget/CapEx limits (15%), talent/skills shortage (11%), and networking lead times (11%) collectively affect more than a third of organizations, compounding the supply and power challenges.

- Regulatory and data issues remain a factor: Regulatory/compliance issues (8%) and data availability/quality (6%) round out the constraint landscape, reflecting growing political challenges around permitting and data residency.

“Cloud service providers are driving unprecedented capital expenditure, but even that spending is running into hard physical limits,” noted Burke. “Power generation is a binding ceiling on hyperscaler expansion, and utility infrastructure timelines measure in years, not quarters. This constraint environment means that organizations must adopt a portfolio approach to chip supply and evaluate hybrid deployment models that span public cloud, on-premises data centers, and colocation facilities.”

Read more in the “2H 2025 Data Center Semiconductors Global Enterprise Decision Maker Survey Report” and “Q2 2025 Data Center Semiconductor Spot Check Report” on the Futurum Intelligence Platform.

About Futurum Intelligence for Market Leaders

Futurum Intelligence’s Semiconductor, Supply Chain, and Emerging Tech IQ service provides actionable insight from analysts, reports, and interactive visualization datasets, helping leaders drive their organizations through transformation and business growth. Subscribers can log into the platform at https://app.futurumgroup.com/, and non-subscribers can find additional information at Futurum Intelligence.

Follow news and updates from Futurum on X and LinkedIn using #Futurum. Visit the Futurum Newsroom for more information and insights.

Other Insights from Futurum:

Orbital Computing Can Reach $1 Trillion Addressable Market by 2030 – Subscribers*

State of the Market Report: Semiconductors, Supply Chain, and Emerging Technology, Q2 2026 – Subscribers*

AI Grid Constraints Will Push Over 33% of Data Centers Off-Grid by 2030

Author Information

Brendan is Research Director, Semiconductors, Supply Chain, and Emerging Tech. He advises clients on strategic initiatives and leads the Futurum Semiconductors Practice. He is an experienced tech industry analyst who has guided tech leaders in identifying market opportunities spanning edge processors, generative AI applications, and hyperscale data centers.

Before joining Futurum, Brendan consulted with global AI leaders and served as a Senior Analyst in Emerging Technology Research at PitchBook. At PitchBook, he developed market intelligence tools for AI, highlighted by one of the industry’s most comprehensive AI semiconductor market landscapes encompassing both public and private companies. He has advised Fortune 100 tech giants, growth-stage innovators, global investors, and leading market research firms. Before PitchBook, he led research teams in tech investment banking and market research.

Brendan is based in Seattle, Washington. He has a Bachelor of Arts Degree from Amherst College.