Austin, Texas, USA, April 21, 2026

The Futurum Group today released the “1H 2026 Intelligent Devices Market Sizing & Five-Year Forecast,” a bottom-up analysis of the global edge silicon market that spans 12 semiconductor suppliers, 11 silicon types, and 7 device destinations from 2022 through 2030.

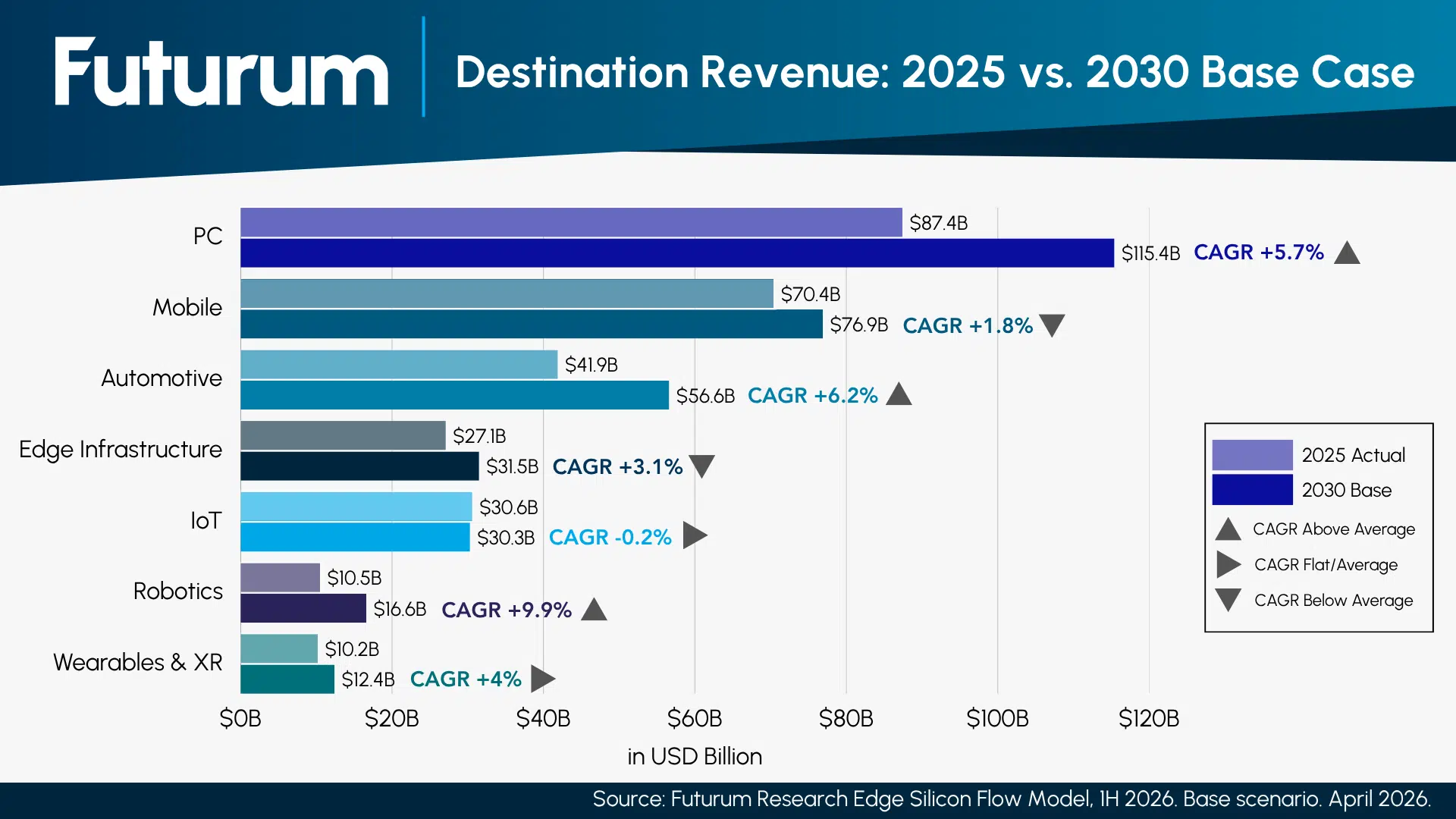

The report finds the edge silicon market at $278.1B in 2025 and on a base-case path to $339.7B by 2030, a 22% gain driven not by uniform expansion but by sharp divergence across destination markets. Robotics emerges as the fastest-growing destination at a 9.9% CAGR, while IoT registers a near-flat -0.2% CAGR, underscoring how different the growth trajectories within the edge silicon market have become.

The destination breakdown serves as the report’s defining analytical lens. PC remains the largest single destination at $87.4B in 2025, with the base case projecting $115.4B by 2030 — a 32% gain anchored by rising NPU silicon content as AI PC adoption broadens beyond premium tiers. Average silicon content per AI PC is forecast to climb from $313 in 2025 to $401 by 2030 in the base scenario, driven by integrated NPU, DRAM, and discrete GPU acceleration. Automotive, at $41.9B in 2025, is the most structurally predictable destination in the edge silicon market — the only one that grows across all three scenarios (base, bull, and bear) — reaching $56.6B by 2030 at a 6.2% CAGR, as EV and ADAS platforms structurally increase semiconductor content per vehicle.

At the growth frontier, Robotics — the smallest destination at $10.5B in 2025 — posts the highest five-year CAGR in the model at 9.9%, reaching $16.6B by 2030. Wearables & XR follows at 4.0% CAGR ($10.2B to $12.4B), and Edge Infrastructure grows steadily at 3.1% ($27.1B to $31.5B). Mobile, the second-largest destination at $70.4B, delivers a modest 1.8% CAGR to $76.9B, constrained by unit-volume saturation in developed markets. IoT is the one destination in structural contraction, moving from $30.6B in 2025 to $30.3B by 2030 (-0.2% CAGR), reflecting ongoing commoditization pressure and silicon consolidation in lower-value device categories. The divergence across destinations reflects fundamental architectural shifts in how and where silicon intelligence is deployed within the edge silicon market.

Figure 1: Destination Revenue: 2025 vs. 2030 Base Case

“The destination-level view is where the edge silicon market story becomes most insightful for investors, suppliers, and OEMs alike,” said Olivier Blanchard, Research Director, Intelligent Devices Practice Lead at The Futurum Group. “Robotics and Automotive are where structural demand is still being built from the ground up. IoT’s near-zero CAGR is not a cycle — it is part maturation signal, part open question about the ROI of investing in local intelligence for those use cases. And PC’s recovery is real, but will depend primarily on how fast AI PC adoption moves from premium to mainstream. The edge silicon market is not one story — it is seven, and they diverge sharply.”

Key Findings

- PC Leads in Absolute Dollar Upside: At $87.4B in 2025, PC is the largest single destination in the edge silicon market and projects the greatest absolute dollar gain through 2030 ($115.4B, +5.7% CAGR). The mechanism is AI PC adoption — average silicon content per unit is forecast to rise from $313 in 2025 to $401 by 2030 as NPU integration moves from premium to mainstream across the PC lineup.

- Automotive – The Only All-Scenario Growth Destination: Automotive silicon demand grows across every modeled scenario — bull ($406.7B total market), base ($339.7B), and bear ($271.8B). At $41.9B in 2025, Automotive reaches $56.6B by 2030 at a 6.2% CAGR, driven by EV and ADAS platform proliferation that structurally increases semiconductor content per vehicle from roughly $400-600 in legacy ICE to over $1,000 in leading EV platforms.

- Robotics – Fastest-Growing Destination at 9.9% CAGR: Robotics is the highest-growth destination in the edge silicon market, expanding from $10.5B in 2025 to $16.6B by 2030. Physical AI platforms, industrial automation, and emerging consumer robotics categories are driving silicon demand in a destination that was negligible in prior market cycles.

- IoT in Structural Reset, Not Cyclical Dip: IoT registers a -0.2% CAGR across the forecast horizon, declining from $30.6B in 2025 to $30.3B by 2030. This is not a cyclical downturn; it reflects structural silicon consolidation in lower-value connected device categories, commoditization pressure on MCU and connectivity silicon, and a market that has absorbed its initial deployment wave without a new architectural driver to sustain growth.

- Mobile Steady but Constrained: Mobile remains the second-largest destination at $70.4B in 2025, growing to $76.9B by 2030 at a 1.8% CAGR. Unit volume saturation in developed markets limits upside even as per-device silicon content rises modestly. Mobile’s share of total edge silicon market revenue is expected to compress from 25.3% in 2025 to 22.6% by 2030 as faster-growing destinations — Robotics, Automotive, PC — expand their relative weight.

The full “1H 2026 Intelligent Devices Market Sizing & Five-Year Forecast Report” is available now for Futurum Intelligence subscribers. Non-subscribers can click here for more information.

About Futurum Intelligence for Market Leaders

Futurum Intelligence’s Intelligent Devices IQ service provides actionable insight from analysts, reports, and interactive visualization datasets, helping leaders drive their organizations through transformation and business growth. Subscribers can log into the platform at https://app.futurumgroup.com/, and non-subscribers can click here for more information.

Follow news and updates from Futurum on X and LinkedIn using #Futurum. Visit the Futurum Newsroom for more information and insights.

Other Insights from Futurum:

Lenovo Q3 FY 2026 Earnings: Broad-Based Growth, AI Mix Rising

HP Q1 FY 2026 Earnings: AI PC Momentum, Memory Costs Temper Outlook

Qualcomm Q1 FY 2026: Record Revenue, Memory Headwinds

Author Information

Olivier Blanchard is Research Director, Intelligent Devices. He covers edge semiconductors and intelligent AI-capable devices for Futurum. In addition to having co-authored several books about digital transformation and AI with Futurum Group CEO Daniel Newman, Blanchard brings considerable experience demystifying new and emerging technologies, advising clients on how best to future-proof their organizations, and helping maximize the positive impacts of technology disruption while mitigating their potentially negative effects. Follow his extended analysis on X and LinkedIn.