Austin, Texas, USA, November 12, 2025

While GPUs Remain the Cornerstone of the Data Center Semiconductor Market, XPUs Are Set To Accelerate

Futurum launches two major reports on the data center semiconductor market, including a market forecast and a survey of key decision-makers focusing on AI data centers.

Futurum Research has released its 2H 2025 Data Center Semiconductor Decision Maker Survey alongside the Q2 2025 Data Center Semiconductor Market Report.

Our latest findings reaffirm that GPUs remain the cornerstone of modern data center buildouts despite the rising momentum of adoption in XPUs. The rapid proliferation of large-scale AI workloads continues to favor GPU-centric architectures—driven by their unmatched software ecosystems, superior performance, and proven scalability, particularly underpinned by NVIDIA’s continued leadership, along with increasingly mature offerings from AMD. Indeed, our latest data indicates that approximately 75% of total compute spending is allocated to GPUs in 2025, compared with 12% for CPUs and 13% for XPUs, highlighting GPUs’ continued dominance in data center investments.

Other data points in our new survey also highlight the acceleration in the usage of XPUs (e.g., TPU, Trainium, and MTIA) as an increasingly critical component within the global data center compute mix. According to our end-user survey, compute spending is expected to increase across all categories in 2026, led by XPUs with an estimated +23% annual growth, outpacing GPUs (+29%) and CPUs (+12%). This shift underscores the emerging strategic role of XPUs in shaping the next generation of AI-centric data center architectures.

These developments occur at a time when the data center semiconductor market is experiencing rapid expansion. According to Futurum’s latest estimate, the global data center compute market is projected to surge from $62 billion in 2022 to $546 billion by 2029, representing an almost ninefold increase and a 29% compound annual growth rate (CAGR).

Our most recent market model aligns with findings from the Decision Maker Survey, indicating that the XPU market is set to accelerate as hyperscalers expand adoption and integrate these chips into broader compute buildouts.

By type of AI accelerator, GPUs continue to dominate, with a market size projected to grow from $13 billion in 2022 to $385 billion by 2029, as AI workloads increasingly depend on GPU acceleration. XPUs are also gaining relevance, expanding from $15.5 billion to $84.0 billion, while CPUs increase from $33.7 billion to $76.6 billion. Overall, compute demand is decisively pivoting toward accelerators, led by NVIDIA, AMD, and custom AI accelerators.

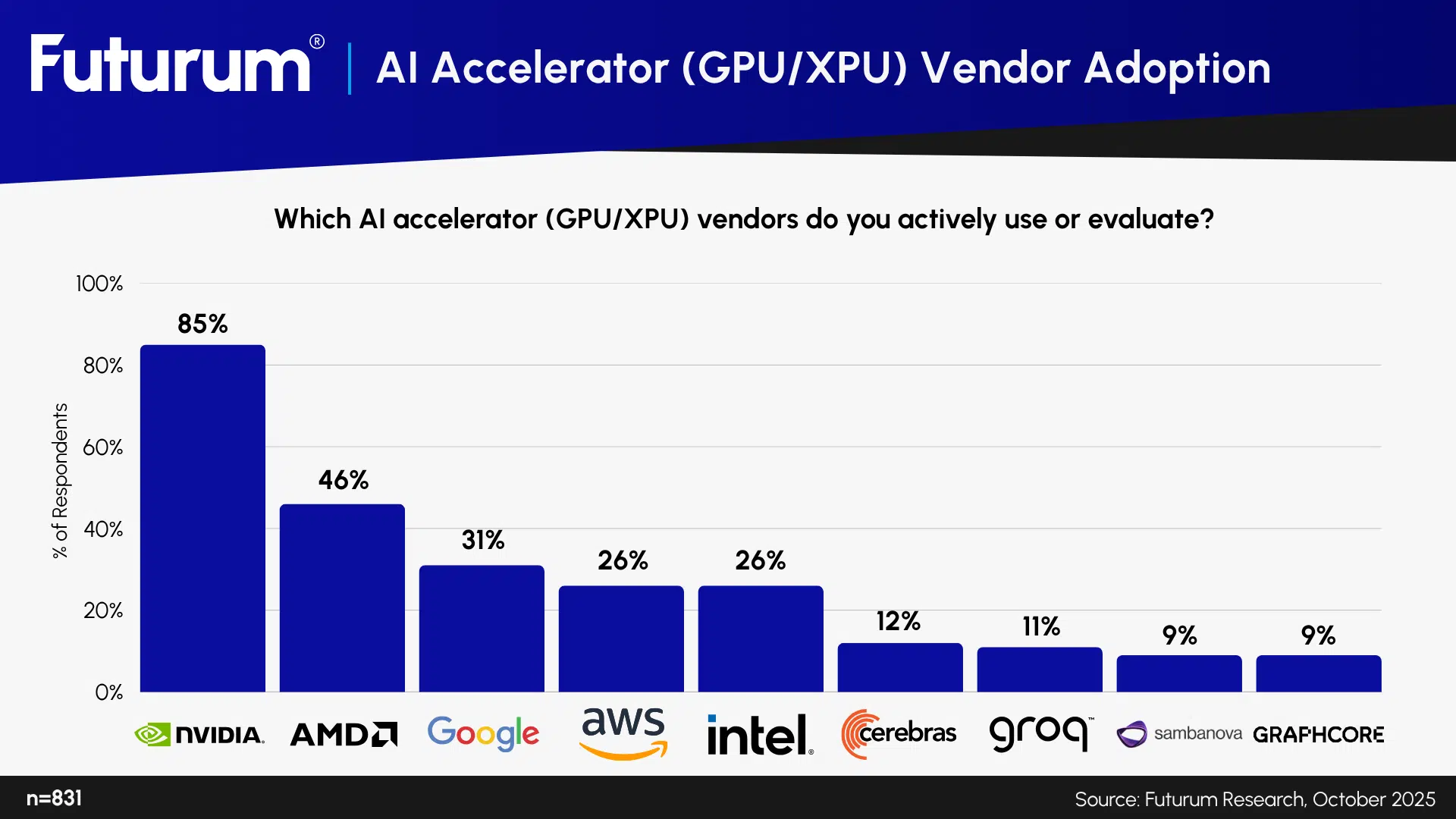

Figure 1: AI Accelerator Vendor Adoption (GPU/XPU)

“While data center operators continue to rely heavily on GPUs from companies such as NVIDIA and AMD, it’s increasingly evident that the adoption of XPUs is accelerating. The commitment among hyperscalers and enterprises to integrate XPUs into their compute infrastructure is strong and growing. This trend does not imply that XPUs will replace GPUs. Rather, as overall compute demand continues to expand rapidly, the total addressable market for compute is rising, creating room for both architectures to thrive, ”said Ray Wang, Research Director for Semiconductors, Supply Chain, and Emerging Technology.

Our research also offers other key data points on the AI data center semiconductor landscape:

- The global data center compute market expands dramatically from $62 billion in 2022 to $546 billion by 2029, reflecting an almost ninefold increase and a 29% CAGR.

- In 2025, GPUs dominate the data center compute market, accounting for $174.7 billion, followed by XPUs ($30.9 billion) and CPUs ($26.8 billion), bringing total spending to $232.4 billion.

- In 2025, GPUs accounted for 58% of compute spending, followed by CPUs (29%) and XePUs (13%). While GPUs remain dominant, XPUs lead growth (+22%), outpacing GPUs (+19%) and CPUs (+14%) in 2026, reflecting increasing adoption in custom AI accelerators alongside sustained demand for GPUs.

- AI workloads are increasingly diversified beyond just training, with balanced training and inference leading (38%), followed by mostly inference (33%), training-dominant (19%), and data prep/ETL-heavy (10%) workloads.

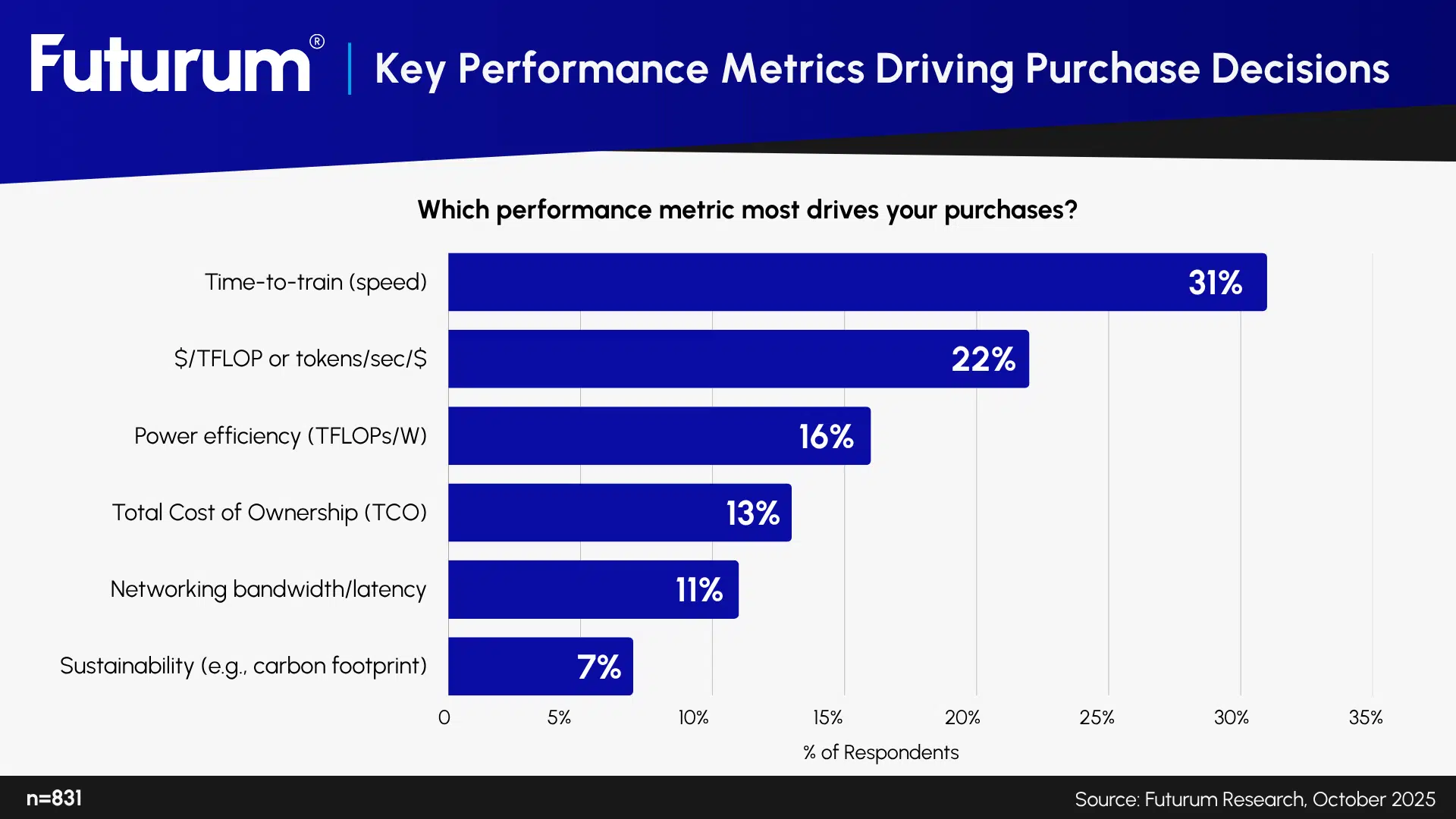

- In terms of key factors influencing compute purchases, speed (time-to-train) is the top driver (31%), followed by cost efficiency ($/TFLOP or tokens/sec/$, 22%) and power efficiency (16%). In comparison, TCO (13%), networking (11%), and sustainability (7%) are lower priorities.

In addition to the silicon finding, our survey also seeks to understand the key drivers and considerations behind the AI data center buildout. For example, our survey identified that AI workloads are becoming more diversified beyond training, with balanced training and inference leading (38%), followed by mostly inference (33%), training-dominant (19%), and data prep/ETL-heavy (10%).

We also found the key factor dictating customers’ speed (time-to-train) is the top factor driving compute purchases (31%), ahead of cost efficiency (22%) and power efficiency (16%), while TCO (13%), networking (11%), and sustainability (7%) rank lower in priority.

Figure 2: Key Performance Metrics Driving Purchase Decisions

“Our comprehensive findings on customers’ considerations behind data center buildouts—as well as detailed data on semiconductors used within these environments—are critical for industry vendors and supply chain participants to shape their future technologies, refine product roadmaps, and realign corporate strategies,” noted Wang.

Read more in the reports “Q2 2025 Data Center Semiconductor Spot Check Report” and “2H 2025 Data Center Semiconductors Global Enterprise Decision Maker Survey Report” on the Futurum Intelligence Platform.

About Futurum Intelligence for Market Leaders

Futurum Intelligence’s Semiconductor, Supply Chain, and Emerging Technology IQ service provides actionable insight from analysts, reports, and interactive visualization datasets, helping leaders drive their organizations through transformation and business growth. Subscribers can log into the platform at https://app.futurumgroup.com/, and non-subscribers can find additional information at Futurum Intelligence.

Follow news and updates from Futurum on X and LinkedIn using #Futurum. Visit the Futurum Newsroom for more information and insights.

Other Insights from Futurum:

AMD OpenAI Partnership: Scale Win or Execution Risk at 6 GW?

Hybrid Bonding at Scale: Powering the Next Era of Semiconductor Packaging

Micron Q4 FY 2025 Earnings Top Estimates on DRAM and HBM Strength

Author Information

Ray Wang is the Research Director for Semiconductors, Supply Chain, and Emerging Technology at Futurum. His coverage focuses on the global semiconductor industry and frontier technologies. He also advises clients on global compute distribution, deployment, and supply chain. In addition to his main coverage and expertise, Wang also specializes in global technology policy, supply chain dynamics, and U.S.-China relations.

He has been quoted or interviewed regularly by leading media outlets across the globe, including CNBC, CNN, MarketWatch, Nikkei Asia, South China Morning Post, Business Insider, Science, Al Jazeera, Fast Company, and TaiwanPlus.

Prior to joining Futurum, Wang worked as an independent semiconductor and technology analyst, advising technology firms and institutional investors on industry development, regulations, and geopolitics. He also held positions at leading consulting firms and think tanks in Washington, D.C., including DGA–Albright Stonebridge Group, the Center for Strategic and International Studies (CSIS), and the Carnegie Endowment for International Peace.