Austin, Texas, USA, December 19, 2025

Futurum Research Reveals GenAI Deployment Split Nearly Evenly Between Public Cloud (22.4%) and Hybrid Environments (20.8%), While Specialized GPU Neoclouds Capture 10.5% Market Share

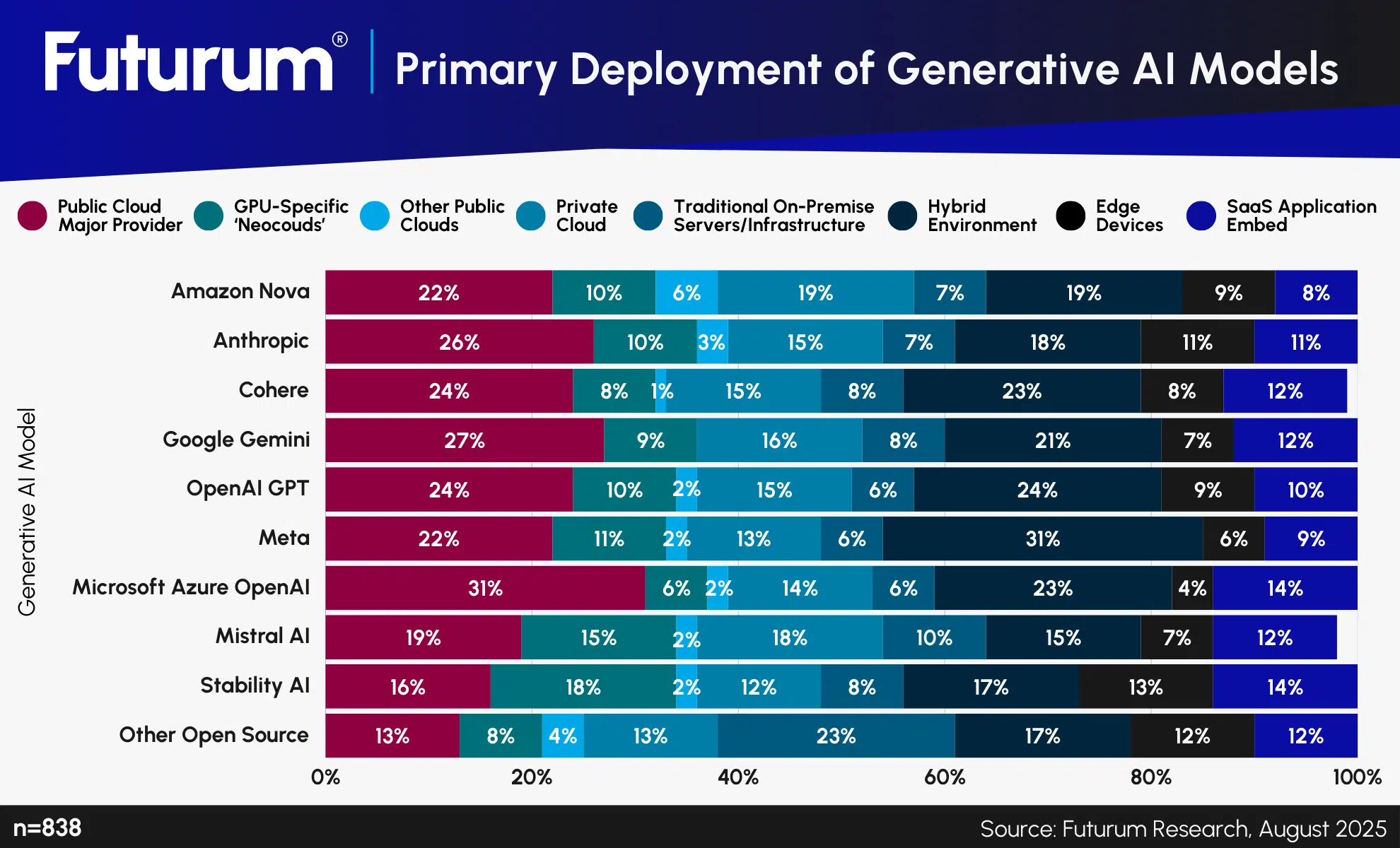

Futurum Group today released comprehensive research mapping generative AI deployment patterns across enterprises, revealing a remarkably balanced distribution between public cloud deployments at 22.4% and hybrid environments at 20.8%. The study, analyzing deployment strategies for ten major GenAI model families, shows organizations are rejecting one-size-fits-all approaches in favor of diverse, model-specific deployment strategies, with Meta’s models leading hybrid adoption at 31% while Microsoft Azure OpenAI Service dominates public cloud at 31%.

The research uncovered that total cloud deployments (including public cloud, neoclouds, and other clouds) account for 35.3% of implementations, while on-premise and private cloud deployments combine for 23.9%, with hybrid environments capturing the remaining 20.8%. This three-way split signals that enterprises are prioritizing flexibility and control over simplicity, choosing deployment models based on specific use cases, compliance requirements, and performance needs rather than defaulting to a single infrastructure approach.

Figure 1: Primary Deployment of Generative AI Models, % Respondents (n=838)

Nick Patience, VP & AI Platforms Practice Lead at Futurum, said, “The near-equal split between public cloud and hybrid deployments – 22.4% versus 20.8% – represents a fundamental shift in how enterprises approach AI infrastructure. Organizations aren’t choosing between cloud and on-premise; they’re orchestrating complex, multi-environment strategies. The fact that no single deployment model captures more than a quarter of implementations shows that GenAI has outgrown the simplistic ‘cloud-first’ narrative that dominated early enterprise AI adoption.”

The research reveals several critical patterns reshaping GenAI infrastructure strategies:

- Deployment Fragmentation: No single infrastructure approach dominates, with the leading deployment method (public cloud) capturing only 22.4% of implementations, indicating that enterprises prioritize architectural flexibility over standardization, tailoring deployments to specific model characteristics and use cases.

- Neocloud Emergence: GPU-specific neoclouds have captured 10.5% of overall deployments, with Stability AI (18%) and Mistral AI (15%) showing particularly high adoption rates, suggesting that specialized infrastructure providers are carving out a significant niche for compute-intensive workloads.

- Model-Specific Strategies: Meta models exhibit the highest hybrid adoption (31%), while Microsoft Azure OpenAI leads in public cloud (31%), indicating that optimal deployment varies significantly by model architecture, licensing, and integration requirements, rather than following universal patterns.

- Open Source Anomaly: Open source models show dramatically different deployment patterns with 23% on traditional on-premise infrastructure – nearly triple the average – highlighting how licensing flexibility enables organizations to maximize existing investments and maintain complete control.

The strength of hybrid deployments, nearly matching public cloud adoption, challenges conventional wisdom about AI infrastructure. Organizations are hedging their bets, maintaining flexibility to move workloads as requirements evolve, costs change, or new regulations emerge. This balanced approach suggests enterprises have learned from previous technology waves that vendor lock-in and single-point dependencies create long-term risks. “The 10.5% share captured by GPU-specific neoclouds is particularly intriguing,” Patience added. “These specialized providers are proving that there’s substantial demand for infrastructure optimized specifically for AI workloads, especially for organizations running models like Stability AI that require intensive compute resources. This represents a new category of infrastructure that didn’t exist five years ago.”

The data also reveals that edge deployments, while averaging only 8.6%, show significant variation by model type. This suggests early movement toward distributed AI architectures, particularly for applications requiring low latency or data locality. Similarly, SaaS-embedded deployments at 11.4% indicate that many organizations are consuming AI capabilities through existing applications rather than building standalone infrastructure.

Subscribers can read more in the “1H 2025 AI Platforms Decision Maker Survey Report” on the Futurum Intelligence Platform. Non-subscribers can click here for more information.

About Futurum Intelligence for Market Leaders

Futurum Intelligence’s AI Platforms IQ service provides actionable insight from analysts, reports, and interactive visualization datasets, helping leaders drive their organizations through transformation and business growth. Subscribers can log into the platform at https://app.futurumgroup.com/, and non-subscribers can find additional information at Futurum Intelligence.

Follow news and updates from Futurum on X and LinkedIn using #Futurum. Visit the Futurum Newsroom for more information and insights.

Other Insights from Futurum:

NVIDIA Bolsters AI/HPC Ecosystem with Nemotron 3 Models and SchedMD Buy

AI Platforms Market $292B by 2030, Mapping Risks & Bull Market Scenarios

Equinix’s Bold Strategy: Doubling Global Data Center Capacity for the AI Era

Author Information

Nick Patience is VP and Practice Lead for AI Platforms at The Futurum Group. Nick is a thought leader on AI development, deployment, and adoption - an area he has researched for 25 years. Before Futurum, Nick was a Managing Analyst with S&P Global Market Intelligence, responsible for 451 Research’s coverage of Data, AI, Analytics, Information Security, and Risk. Nick became part of S&P Global through its 2019 acquisition of 451 Research, a pioneering analyst firm that Nick co-founded in 1999. He is a sought-after speaker and advisor, known for his expertise in the drivers of AI adoption, industry use cases, and the infrastructure behind its development and deployment. Nick also spent three years as a product marketing lead at Recommind (now part of OpenText), a machine learning-driven eDiscovery software company. Nick is based in London.